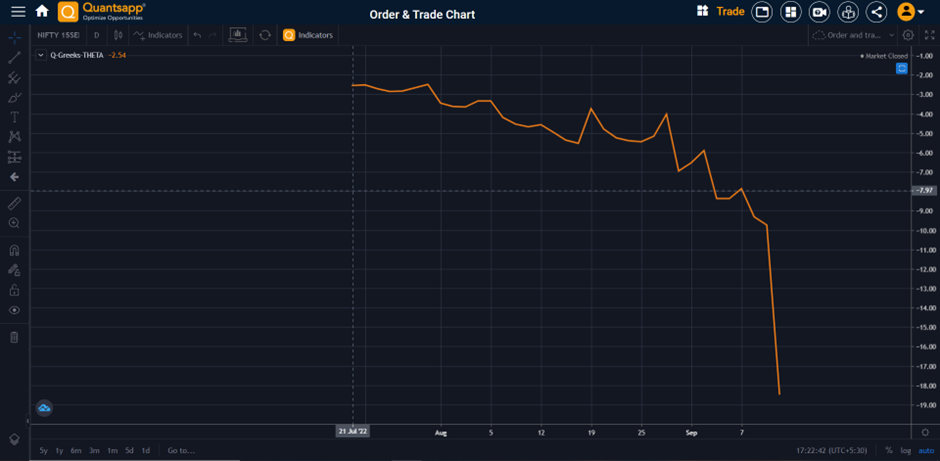

The need for 3-Leg Directional Strategy is because of the pace of Time Value Decay (or Theta Decay). The chart below shows how Theta impacts as Expiry date nears. Theta or 1 day drop in premium was 2.5 at the beginning of the chart and went to -18 (7x) in a matter of just 2 weeks.

Ideas

Ideas

.svg)

Intel Junction

Trade

Trade

Orders API

Watchlist

Orders

Positions

Broker Access

Hot Keys

Alert Trigger Order (ATO)

Bracket Order

Target Stoploss Order

Add Broker

Track

Futures OI

Options OI

News

Price & Volume

Alerts

Built-Up Breadth

Built-Up Scrip Symbol

Synopsis Futures OI

Built-Up Sectors

Top Stocks

Intraday Movers

Analyze

Charts

IV

PCR

Expiry

Price & Volume

Charts/ Order & Trade

Multi Strike OI

O&T Watch List

Strategy Chart

Scan

Hist-Futures

Hist-Options

Pairs

Built-Up Scrip OI-Historical

Built-Up Sector Cycle

Built-Up Sector OI-Historical

Built-Up Scrip Cycle

Comparative Analysis

Tools

Easy Strategy

Strategy Builder

Quant Models

Essential Tools

Optimizer Find Strategy

Optimizer Find Specific

Optimizer My Forecasts

Optimizer Constrains

Learn

Live

Self Learning

Events

Webinars

Book a Session

Chapter 5

3 - leg directional strategies

To Safeguard from this Traders use Ratio Spreads. Let us understand what they are.

Ratio Spread

A ratio spread is a neutral options strategy in which an investor simultaneously holds an unequal number of long and short or written options. The long positions in options and the short positions are established in a pre-specified ratio. The most common ratio is that there are two shorts for every long position in options. All the options are of the same type, for the same underlying, but different strikes.

Traders use a ratio strategy when they believe the price of the underlying asset won't deviate much from the current market price. Call ratio spread is used, when the trader is slightly bullish, while put ratio spread is used, when the trader is slightly bearish.

Ratio Call Spread

A call ratio spread involves buying one at-the-money (ATM) or out-of-the-money (OTM) call option, while also selling or writing two call options that are further OTM (higher strike). The max profit for the trade is the difference associated with the long and short strike prices, plus the net credit received. For the call ratio spread, a loss occurs if the price makes a larger move to the upside as the trader has sold more positions than they have long.

Consider a call ratio spread where Nifty Futures Fair value is quoting at 18,010, trader shall

Buy 18000 3 Nov 2022 CE at 110

Sell 18200 3 Nov 2022 CE at 31.40 (2 lots)

The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 18,047 and Expiry BEP2 is at 18,353.

The loss occurs below expiry BEP1 and above expiry BEP2; while the maximum profit of the Nifty occurs at about 18,200, where the second leg and third leg are positioned. It is the difference between the two strikes * lot size – total premium paid for the strategy.

Ratio Put Spread

A put ratio spread involves buying one at-the-money (ATM) or out-of-the-money (OTM) put option, while also selling or writing two put options that are further OTM (higher strike). The max profit for the trade is the difference between the long and short strike prices, plus the net credit received. For the put ratio spread, a loss occurs if the price makes a large move to the upside because the trader has sold more positions than they have long.

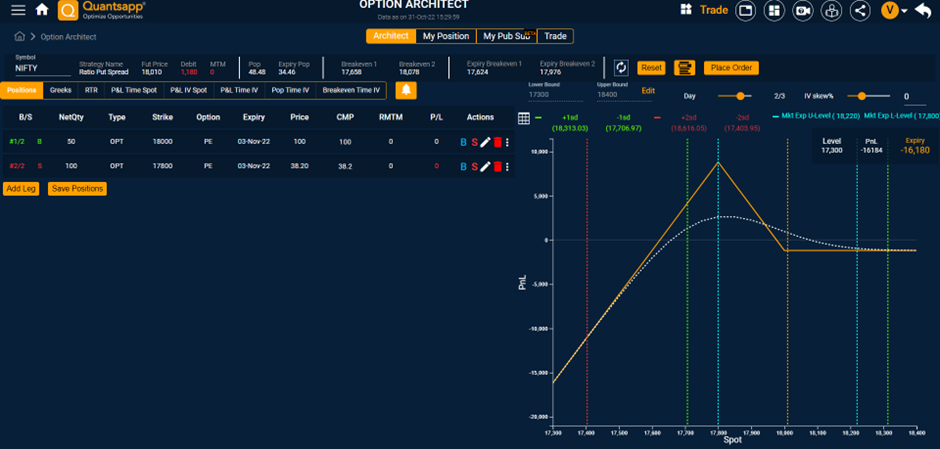

Consider a put ratio spread where Nifty Futures Fair value is quoting at 18,010, trader shall

Buy 18000 3 Nov 2022 PE at 100

Sell 17800 3 Nov 2022 PE at 38.20 (2 lots)

The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,624 and Expiry BEP2 is at 17,976, as available on the screen of Quantsapp.

The loss occurs below expiry BEP1 and above expiry BEP2; while the maximum profit of the Nifty occurs when at about 17800, where the sell legs of the put option are present. It is the absolute difference between the two strikes * lot size – total premium paid for the strategy.

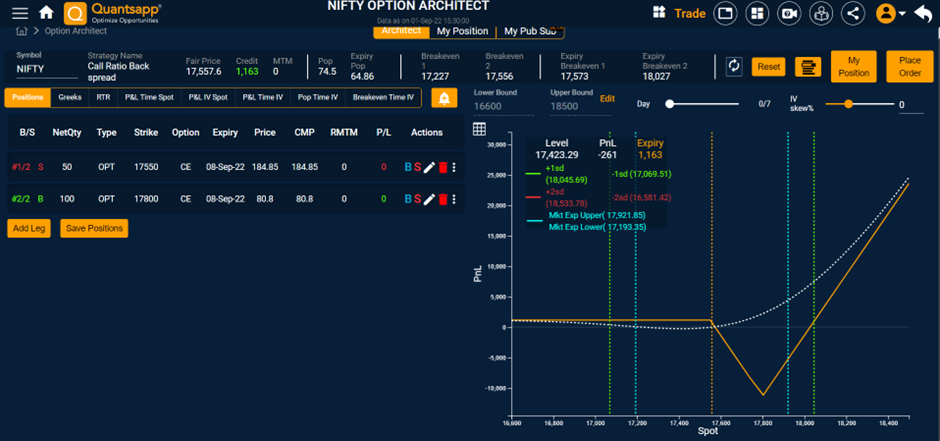

Call Ratio Back Spread

Call Ratio back spread is extremely bullish strategy that expects high volatility in the stocks. It requires sharp upward move in the stock.

Call Ratio Back spread is a bullish strategy that is formed by Selling 1 lot ATM Call and Buying 2 lots OTM call. The net cost to establish the strategy is very low, as it involves selling of one option and buying of two cheaper options. Maximum Profit is unlimited if the stock moves above higher strike call. Maximum loss is difference between the two strikes plus net outflow or less net inflow.

The reduced cost of formulating the strategy. In scenario where implied volatility of call is rising, it provides limited risk and generates high return in scenario where stock gives exponential move in the desired direction. Loss could be higher if the stock doesn’t give desired move. Not meant for an intermediate trader. Time decay could be harmful to the strategy as we are net long. The right strike selection is a key factor for success of this strategy.

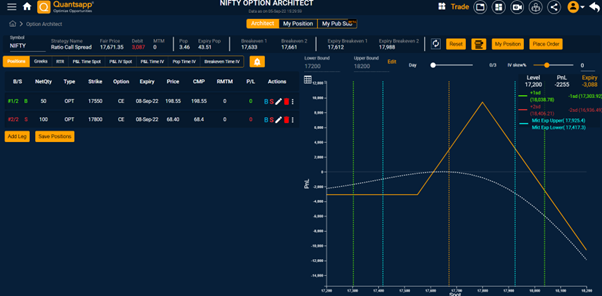

Consider a call ratio backspread where Nifty Futures Fair value is quoting at 17,558, trader shall

Buy 17800 8 Sep 2022 CE at 80.80 (2 lots)

Sell 17550 8 Sep 2022 CE at 184.85

It’s a net credit strategy with premium inflow of about Rs 1,163, as also indicated in the tool of Quantsapp. The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,573 and Expiry BEP2 is at 18,027.

The loss occurs above expiry BEP1 and peaks close to strike price of the other legs of the strategy of about Rs 11,174; while the maximum profit of the Nifty option strategy on expiry is unlimited and depends on how high the underlying Nifty moves.

Put Ratio Back Spread

Put Ratio back spread is extremely Bearish strategy that expects high volatility in the stocks. It requires stock to plummet sharply. Put Ratio Back spread is an extremely bearish strategy that is created with little or no net cost thereby reducing overall risk. It requires aggressive downward move in the stock. The strategy entails selling 1 ATM Put and buying 2 OTM Put. Net cost to establish the strategy is very low. Maximum Profit is unlimited if the stock moves below lower strike Put. Maximum loss is difference between the strikes plus net outflow or less net inflow. The strategy is formulated with lower strategy and generates higher return in the scenario when the stock falls exponentially. The loss could be higher if the stock doesn’t give desired downward movement. Time decay could be harmful to the strategy as we are net long.

FAQs

What is ratio spread strategy?

A ratio spread strategy is where unequal number of options, of a particular type (call or put) are bought and sold across strike prices, for the same underlying.

What are spread strategies?

Spread strategies are typically option strategies which involve buying and selling of an option type of different strikes, of the same underlying and same expiry (unless we are discussing about horizontal spreads). The buy and sell positions may be in a ratio of 1:1 or 1:2, so on.

Is ratio spread profitable?

Ratio spread is typically a mild directional bet on the stock, where option trader expects prices to rise/fall moderately till the price point where the options legs were sold, in case of call/put ratio spread.

What is a 1 by 2 call spread?

The 1 x 2 call spread is created by the buying of one lot of call option at a lower strike price and selling 2 lots of call option of the same underlying at a higher strike price.

What is a 1 by 2 put spread?

The 1 x 2 put spread is created by the buying of one lot of put option at a higher strike price and selling 2 lots of put option of the same underlying at a lower strike price.