The Strip is high volatility strategy with a downside bias. Strip is neutral to bearish Strategy; Ideal for traders who are anticipating an increase in volatility with the stock price moving explosively in either direction, preferably on the downside.

It involves the purchase of 1 lot ATM call and 2 lots of ATM puts with same expiry. The strategy is expensive as compared to a straddle, as there is a purchase of 3 legs of options and the expectation is of an explosive move on the downside.

The maximum Profit is unlimited. However, the profit is more skewed on downside as double the number of puts are bought. Profitability improves at double the speed on downside. The BEP on the upside is the strike plus the net debit, which is more than the Straddle because we have bought double the amount of puts. It is Net debit Strategy as you have bought both Call & Put. Strip is more expensive than usual Straddle because of the extra Put within the strategy.

Time decay is harmful to Strip. Time decay accelerates exponentially in last week of expiry.

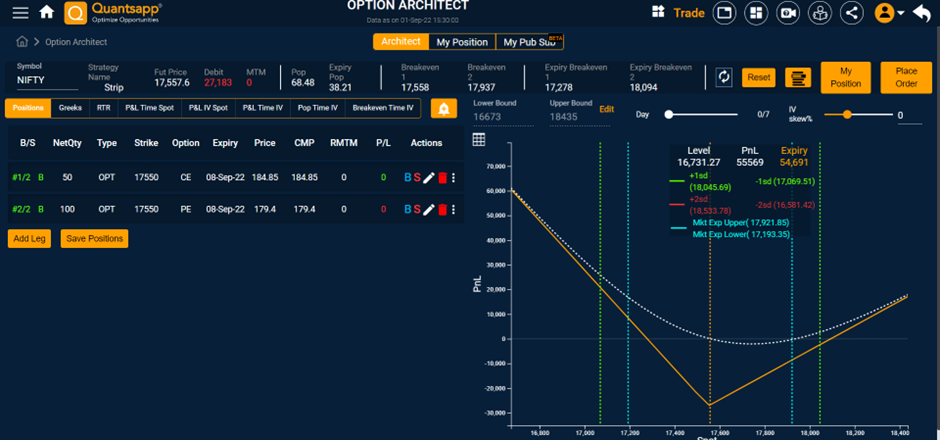

Consider a buy Strip where Nifty Futures Fair value is quoting at 17,558, trader shall

Buy 17550 8 Sep 2022 CE at 184.85

Buy 17550 8 Sep 2022 PE at 179.40 (2 lots)

It’s a net debit strategy with premium outflow of about Rs 27,183, as also indicated in the tool of Quantsapp, i.e. sum of the two put option premia and call option premium, which are bought. The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,278 and Expiry BEP2 of the strategy is at 18,094.

The potential of unlimited profits exist, above the BEPs indicated.

.svg)