.svg)

A bull spread is created when the underlying view on the market is bullish, but not extremely bullish. Considering this situation, the trader would also like to buy a call option (to capture the bullish stance) but would also, not want to spend on option premium, so to avoid the steep option premium cost, would like to take a contrary position in call options. Only a purchase of a naked call means, expectation of a rapid bullish move in Nifty or the underlying, but if the bullish view going to take time to materialise, then the contrary position in call option of a different strike can help protect the overall NSE option strategy from a drop in time value of the option. (also, referred to as theta decay, in options Greek terminology, which shall be explained later).

So, the trader buys a call position with lower strike and sells a call option with higher strike. As lower strike call will cost more than the premium earned by selling a higher strike call, although the cost of position reduces, the position is still a net cash outflow position to start with. A net debit spread strategy, as it is also called. This is what is commonly known as Bull Call Spread.

Secondly, as higher strike call is shorted, all gains on long call beyond the strike price of short call would stand negated by losses of the short call, i.e. if the prices of the underlying Nifty or F&O stock were to rise beyond the strike price of the short call, the profits would flatten out, as the gains from the buy option position would stand negated from the sell position. Hence the profits in this strategy are limited and the loss also is limited to net premium outflow, if prices of Nifty or F&O stock (underlying) were to fall below the strike price of the long call.

The higher strike price, at which the second leg of the strategy is executed can be varied, but one has to remember, higher the strike price, lower is its call premium and lesser the premium inflow from this specific short leg.

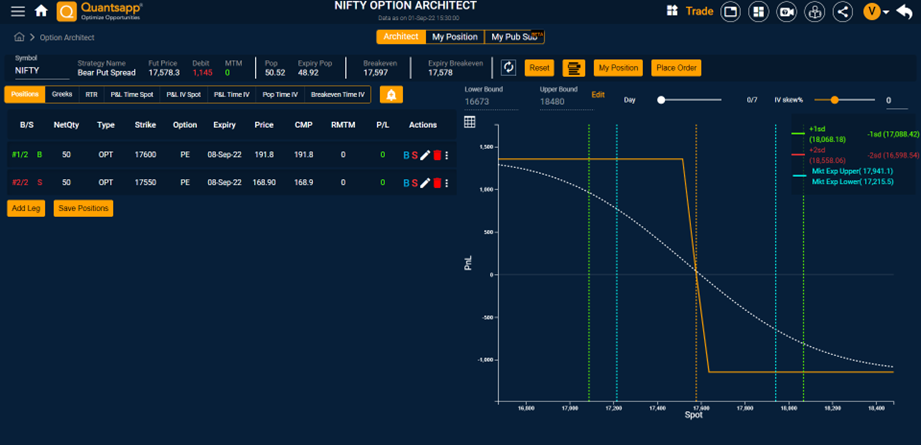

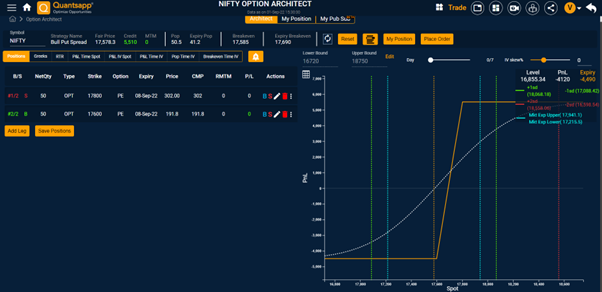

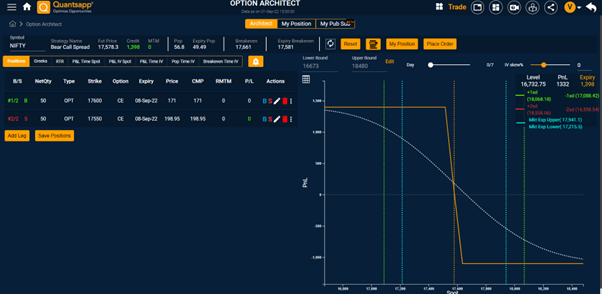

Quantsapp option architect helps traders formulate varied option strategies. Consider a bull call spread where Nifty Futures fair value is quoting at 17578, trader shall

Buy 17600 8 Sep 2022 CE at 171

Sell 17800 8 Sep 2022 CE at 87

It’s a net debit strategy with premium outflow of about Rs 4,200, as also indicated in the tool of Quantsapp. The expiry payoff is indicated in orange colour. Expiry BEP of the strategy is at 17,684.

The maximum loss begins at about Nifty level of 17,600 and is about Rs 4,200; while the maximum profit of the Nifty option strategy is at 17,800 and thereafter, which is capped at Rs 5,800.