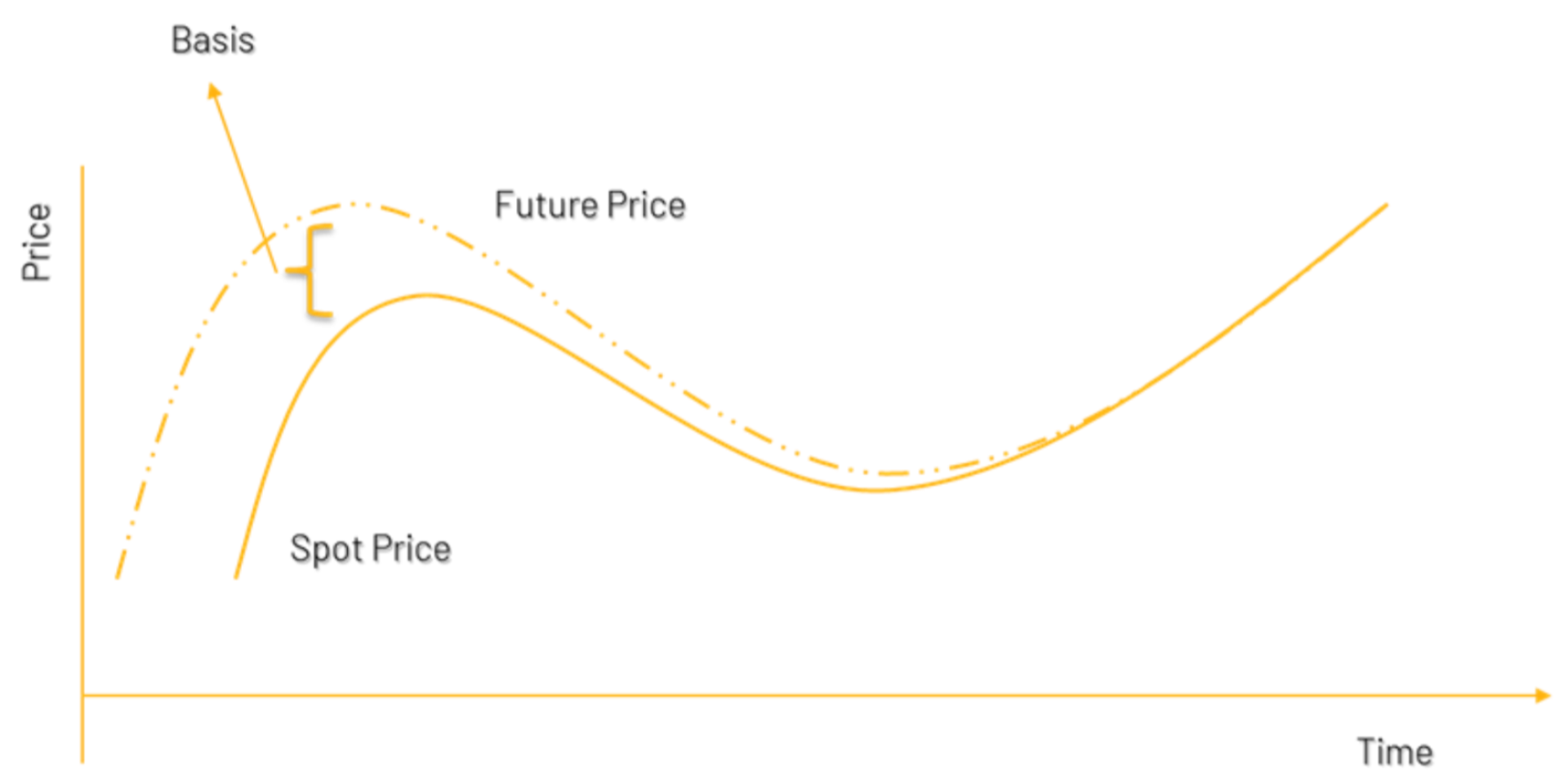

Cost of Carry model defines the relationship between futures prices and spot prices. It measures the warehousing/storage cost (in commodity markets) plus the interest cost associated with carrying the asset till expiration of the futures contract. Of course, other income during the holding period of the futures contract, is subtracted from the cost of carry. Underlying asset like securities (equity or bonds) may have certain inflows, like interest on debt instruments and dividend on equity, during the holding period. For equity derivatives, carrying cost is the interest paid to finance the purchase, reducing dividend earned, as dividend is income and cost of carry is an outgo.

Therefore, the formula for Futures, considering the cost of carry model can be written as:

Ideal Price of Futures = Spot + Cost of Carry – Inflows

F = S*(1+r-q)t

Where F is fair price of the futures contract, S is the Spot price of the underlying asset, q is expected return during holding period t (in years) and r is cost of carry. Note that r and q are annualised figures in percentage. This formula can also be used to evaluate the ideal Nifty future price.

.svg)