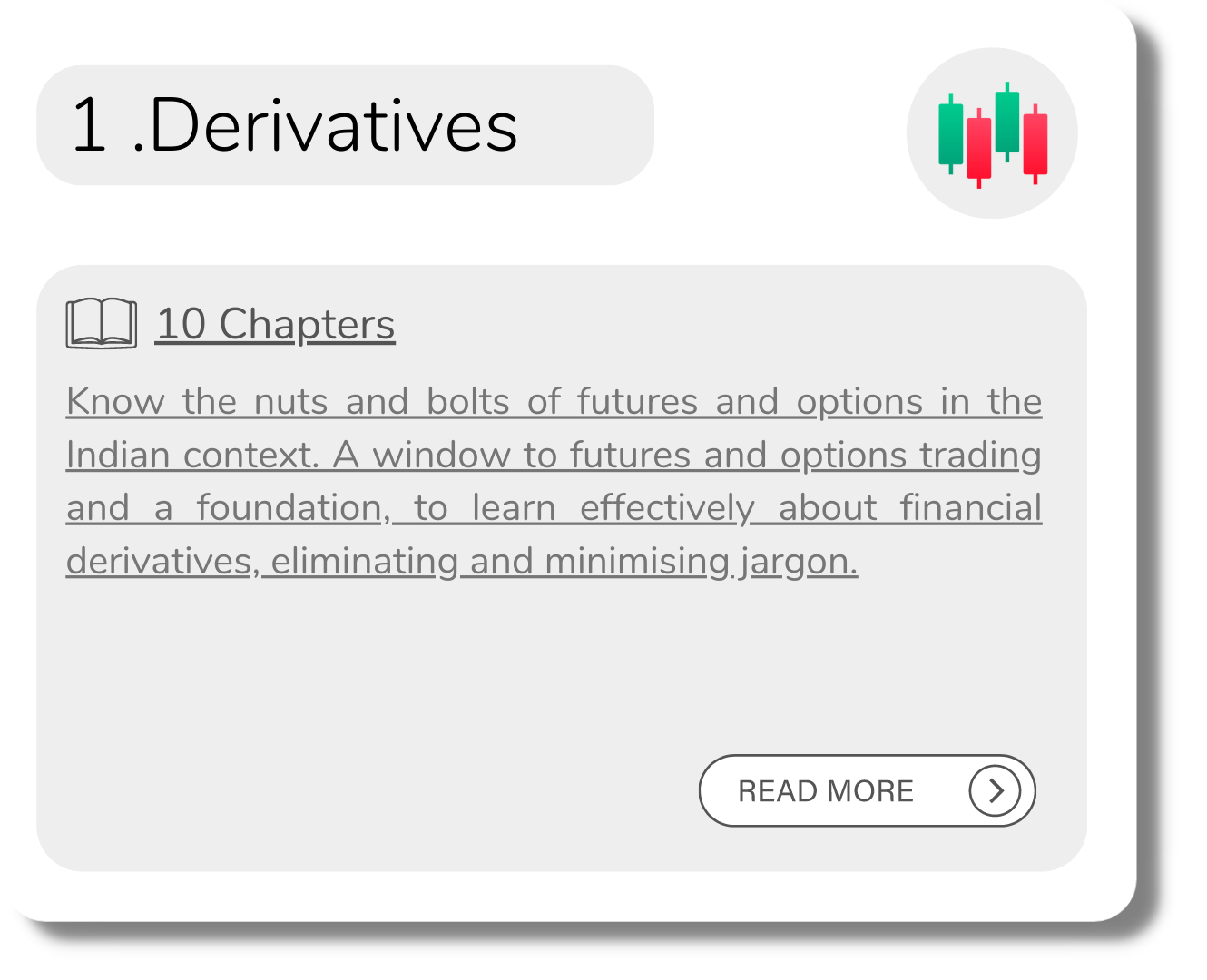

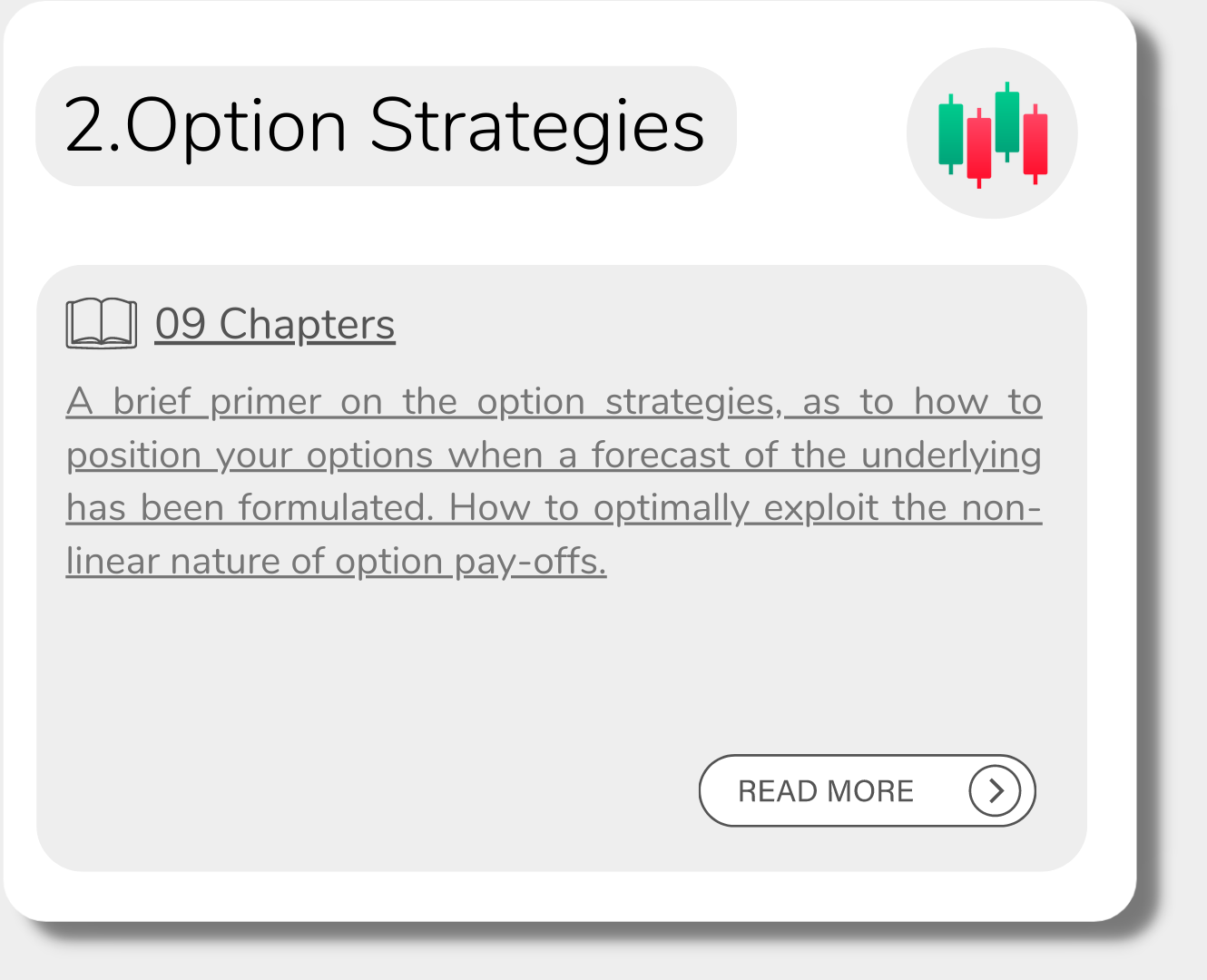

No jargon, just knowledge and practical insights from years of experience in the derivatives market, ready to be applied in Futures & Options Trading

Ideas

Ideas

.svg)

Intel Junction

Trade

Trade

Orders API

Watchlist

Orders

Positions

Broker Access

Hot Keys

Alert Trigger Order (ATO)

Bracket Order

Target Stoploss Order

Add Broker

Track

Futures OI

Options OI

News

Price & Volume

Alerts

Built-Up Breadth

Built-Up Scrip Symbol

Synopsis Futures OI

Built-Up Sectors

Top Stocks

Intraday Movers

Analyze

Charts

IV

PCR

Expiry

Price & Volume

Charts/ Order & Trade

Multi Strike OI

O&T Watch List

Strategy Chart

Scan

Hist-Futures

Hist-Options

Pairs

Built-Up Scrip OI-Historical

Built-Up Sector Cycle

Built-Up Sector OI-Historical

Built-Up Scrip Cycle

Comparative Analysis

Tools

Easy Strategy

Strategy Builder

Quant Models

Essential Tools

Optimizer Find Strategy

Optimizer Find Specific

Optimizer My Forecasts

Optimizer Constrains

Learn

Live

Self Learning

Events

Webinars

Book a Session

Quantsapp Classroom

Quantsapp Classroom

No jargon, just knowledge and practical insights from years of experience in the derivatives market, ready to be applied in Futures & Options Trading

Modules

Modules

Available on