.svg)

The stock exchange acts as a counterparty to the buyer of futures contract and also as a counterparty to the seller of the same futures

contract and also as a counterparty to the seller of the same futures contract; so to safe guard itself from default risk by either of the parties, it charges margins to its brokers for their respective clients. Stock brokers in turn charge margins to clients for placing trades in the Futures & Options segment.

In order to buy 1 lot of futures contract one needs to pay only a small percentage of the total value of the contract. This percentage is called initial margin and is dependent on the volatility of the underlying. The lot size of the futures contract, which specifies the number of shares that comprise 1 lot of that futures contract is pre-determined and mentioned in exchange circulars, based on volatility of the underlying assets. Exchange is likely to charge higher initial margin for underlying assets with higher volatility.

Futures contracts also possess another important margining characteristic, namely, Marking to Market Margin (MTM), which is calculated daily on end of day basis, taking into account the transaction price and closing price. In futures market, the contracts have maturity of several months, profits and losses are settled on day-to-day basis. For a buyer the MTM is computed as Closing price - transaction price; while MTM for a seller is computed as Transaction price – Closing price on the trade or transaction day.

On other days, the additional MTM margin is calculated for a buyer using Today’s close – Yesterday’s close. The seller’s additional MTM is calculated as Yesterday’s close – Today’s close.

In other words, it’s the daily debit and credit which happens on the client’s ledger on the basis of notional profit or loss, his position is in.

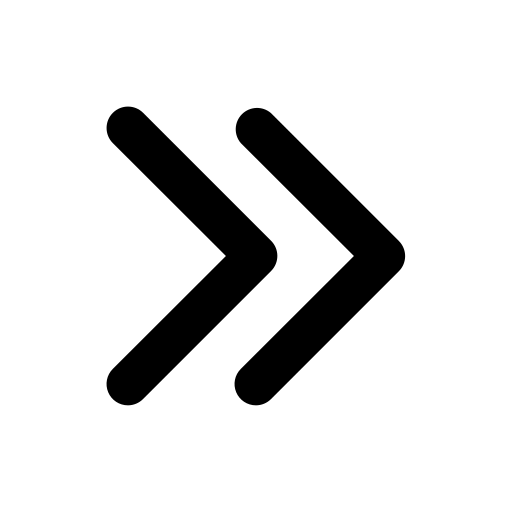

For example:

Buying price of Nifty Futures is 16,000

Selling price of Nifty Futures, when the position is sold is 16,500

The profit on the trade (Assuming lot size = 50) is (16500-16000) *50=Rs 25000/- per lot.

Let’s assume the futures position was held for 4 days and the closing price of Nifty futures on the four days was 16100, 16050, 16250, 16550 respectively. Also, lets assume that the buy transaction of Nifty (1 Lot of futures) was taken on Day 1 at Transaction price1 of 16000 and the sell transaction was done on Day 4 at Transaction price2 of 16500.