Implied volatility is an attribute that is given to any unexplained price change of option premium after passage of stipulated time and stipulated move. Let’s take an example to understand it.

Ideas

Ideas

.svg)

Intel Junction

Trade

Trade

Orders API

Watchlist

Orders

Positions

Broker Access

Hot Keys

Alert Trigger Order (ATO)

Bracket Order

Target Stoploss Order

Add Broker

Track

Futures OI

Options OI

News

Price & Volume

Alerts

Built-Up Breadth

Built-Up Scrip Symbol

Synopsis Futures OI

Built-Up Sectors

Top Stocks

Intraday Movers

Analyze

Charts

IV

PCR

Expiry

Price & Volume

Charts/ Order & Trade

Multi Strike OI

O&T Watch List

Strategy Chart

Scan

Hist-Futures

Hist-Options

Pairs

Built-Up Scrip OI-Historical

Built-Up Sector Cycle

Built-Up Sector OI-Historical

Built-Up Scrip Cycle

Comparative Analysis

Tools

Easy Strategy

Strategy Builder

Quant Models

Essential Tools

Optimizer Find Strategy

Optimizer Find Specific

Optimizer My Forecasts

Optimizer Constrains

Learn

Live

Self Learning

Events

Webinars

Book a Session

Chapter 2

What is Implied Volatility?

Let’s assume:

-

-

-

- Nifty is expected to move from 18500 to 18600 in 2 days, while ideally it is assumed option premium should move from 110 to 150.

- However, does this move really materialise? No!

- Instead, one could witness a gyration possibly from 110 to 160, which implies that the extra Rs 10 increase is due to rise in implied volatility.

- Similarly, one could witness a gyration of Nifty option premium from Rs 110 to Rs 145, which implies that there was a deficit of about Rs 5 from the ideal case. This suggests there has been a drop in implied volatility of the option under study.

-

-

Calculation of implied volatility

Implied volatility is calculated from the market price of options, using the Black Scholes option pricing model. This is the volatility input, which causes the option pricing model to give out the ideal price of the option, which matches the market price of the options.

Black Scholes Option pricing model is dependent on the following:

-

-

-

- Underlying Price.

- Strike Price

- The time to expiration

- Volatility

- Risk-free interest rate

-

-

Implied volatility is calculated by taking the market price of the option, plugging it into the Black-Scholes formula, and solving iteratively for the matching volatility (i.e. implied volatility). Thus Volatility Implied by Options Premium is called Implied Volatility.

Option calculator is a tool of Quantsapp which helps option traders to observe the implied volatility figure from the market price of options of underlying like Nifty or other NSE F&O stocks.

Implied volatility of NIFTY 18450 1Dec2022 CE has been calculated using Quantsapp calculator.

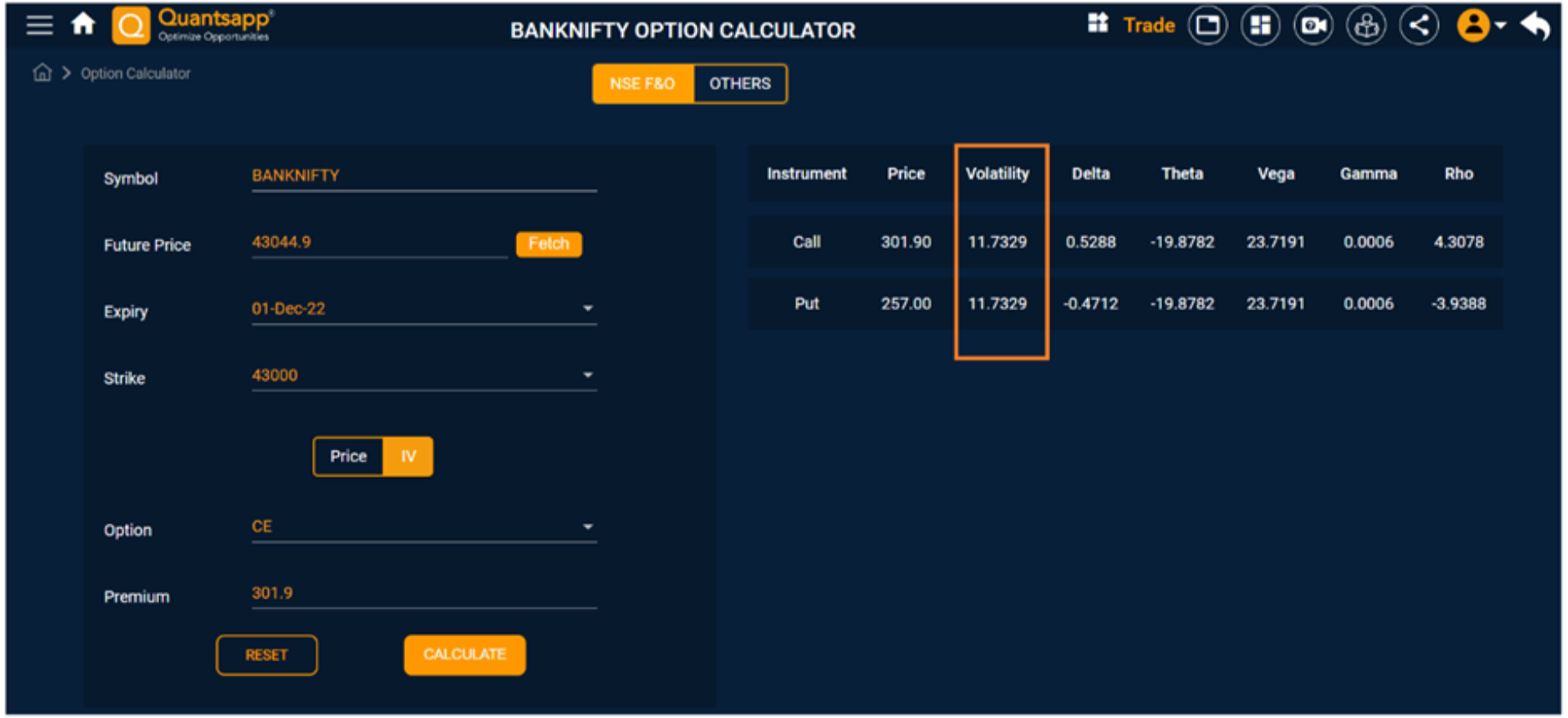

Implied volatility of BANKNIFTY 43000 1Dec2022 CE has been calculated using Quantsapp calculator. Option Greeks are also computed, which shall be discussed later.

Relationship of Implied Volatility and option premium

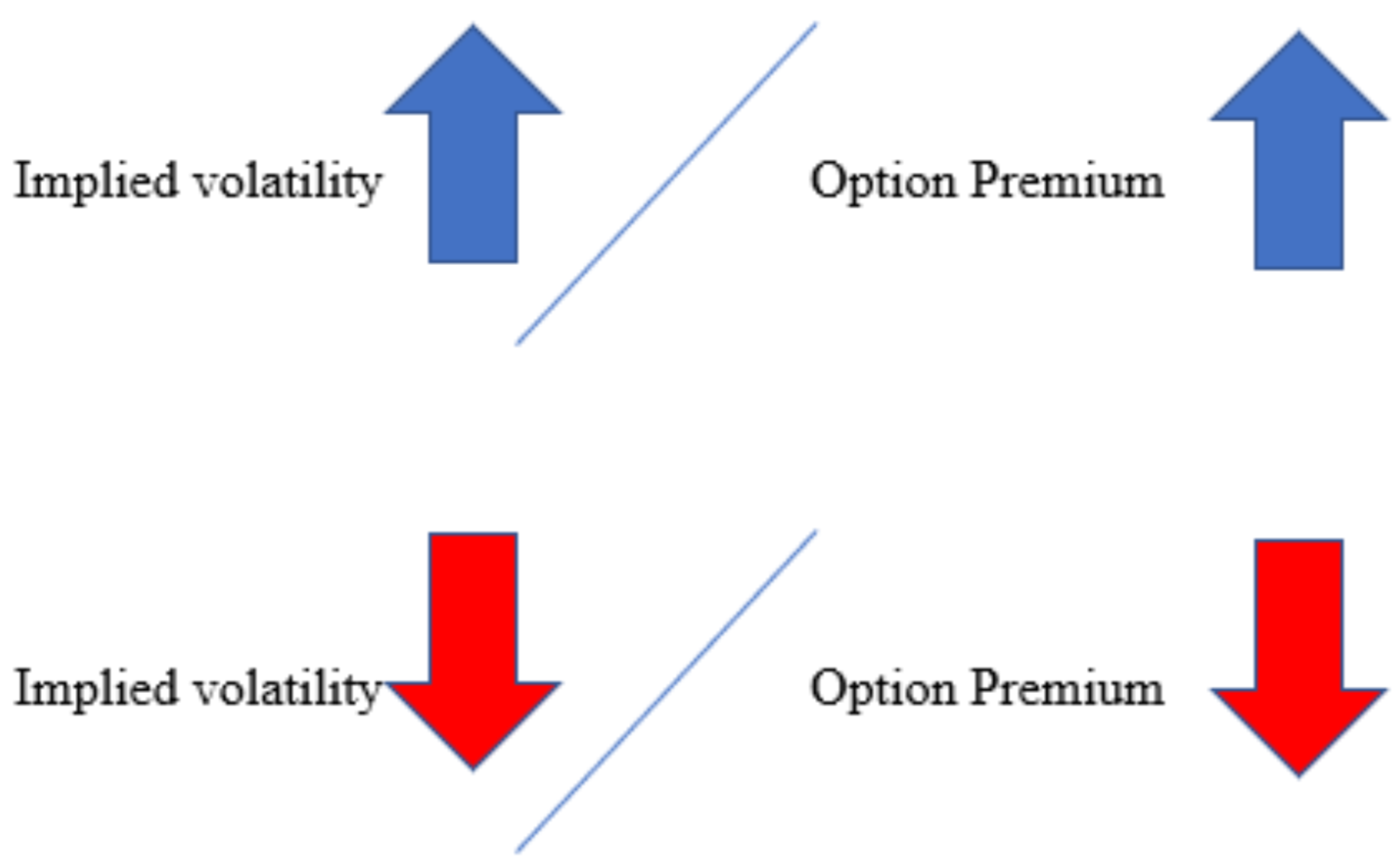

Implied volatility is a measure of uncertainty, which means as uncertainty of an underlying increases, the tendency of traders, fund managers to mitigate their risk/uncertainty would buy options, resulting in increased demand for those options, resulting in a skew in supply/demand situation for the financial instrument under purview. The rise in implied volatility occurs in a symbiotic manner with the increase in option premium. So, options with high levels of implied volatility will result in high-priced option premiums as compared to the same options if the implied volatility was lower.

Relationship of Implied Volatility and option premium

Implied volatility, generally, traders do believe in quotation in and around realised volatility. Then, why and what is the difference between realised a. k. a. historical and implied volatility?

Volatility figure, which is an input in the option calculator that gives rise to prevailing market price of the option expected volatility and not historical volatility (which has gone by). It is option traders’ expectation of upcoming volatility.

As a result, we witness that the expectation of volatility or implied volatility is different for the same stock with different expiries, different option types and different strikes as well.

What do we attribute this difference between the two volatilities to?

Implied volatility = Historical volatility + volatility Risk premium

Let’s consider scenarios which help in understanding varied volatility risk premia. Is the risk going to be higher or lower in coming days?

Scenario 1:

Consider the results of the stock or underlying is about to be released in a couple of days, expected risk premium builds up on uncertainty about results, which could result in sharp moves/price gyrations (fireworks) in the underlying. So implied volatility jumps to about 30%, higher than historical volatility which at that juncture is 10% only.

Implied volatility (30%) = historical volatility (10%) + volatility risk premium (20%)

Scenario 2:

Consider the results of the stock have gone by, now the uncertainty is out of the window. The risk is expected to degrow, so we witness degrowth in implied volatility which is option traders’ perspective of expected volatility, which will drop, due to aforementioned reasons. Volatility risk premium drops, as implied volatility drops to 10%, post result announcement, as traders expect a lull now. However, the recent turbulent times gone by will keep the historical volatility high.

Implied volatility (10%) = historical volatility (30%) + volatility risk premium (-20%)

Some real life examples:

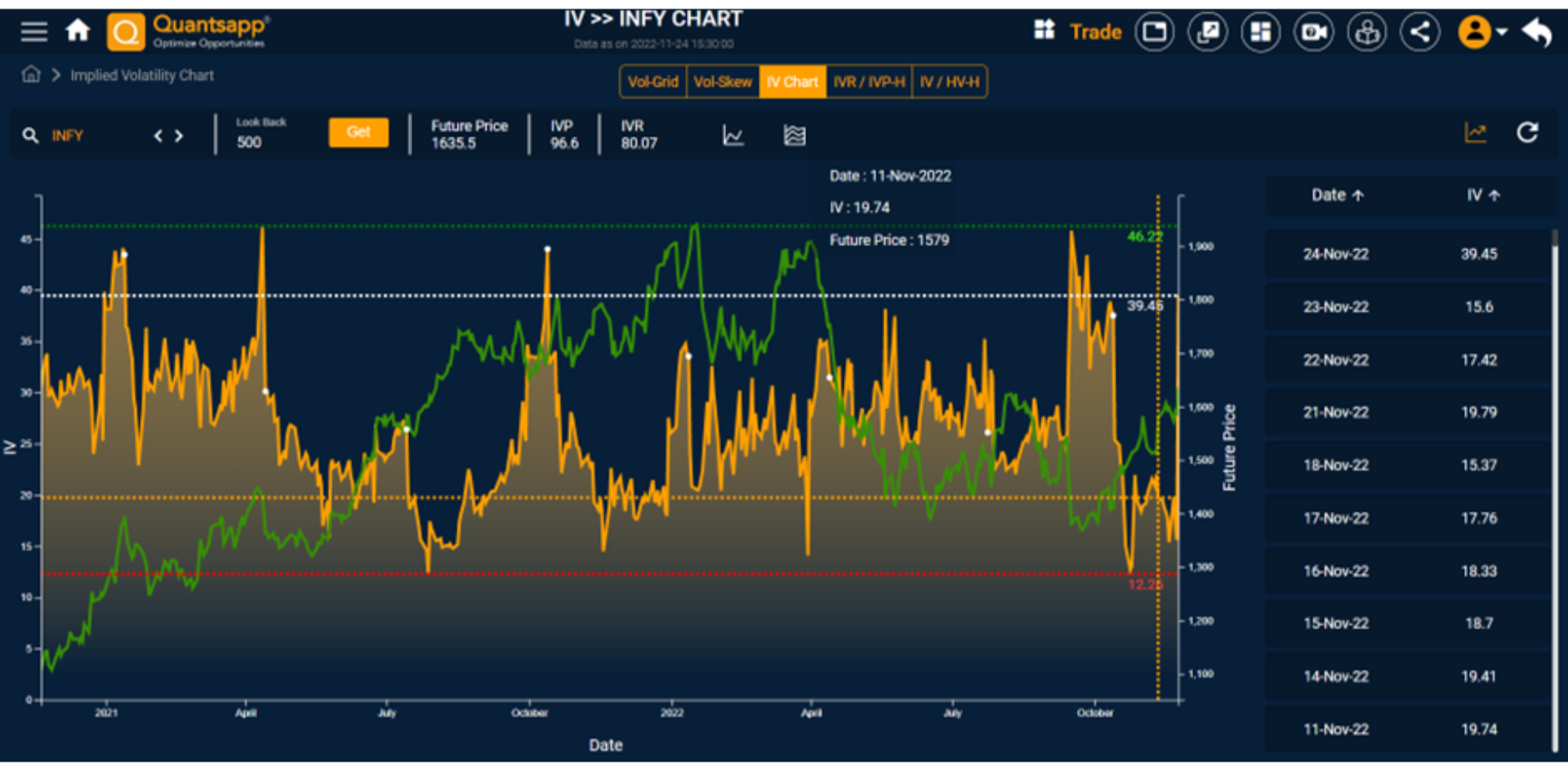

Chart of Infosys Implied Volatility (IV), with white spots indicate Result announcement dates. (Note the spike before result and dissipation after result announcements).

Chart of Nifty Implied Volatility (IV) and Historical Volatility (HV). Note how in 2 major highlighted situations Implied Volatility rose first then dropped while Historical volatility rose later and dropped later.

FAQs

Why Is Implied Volatility Important?

Implied volatility is the market participants’ option-based volatility measure; in other words, it is market’s forecast of volatility of an underlying like Nifty, Bank Nifty and F&O stocks.

How Is Implied Volatility Computed?

Implied volatility is calculated from the market price of options, using the Black Scholes option pricing model.

What is the difference between VIX and implied volatility?

VIX is a volatility index, while implied volatility is market’s perception of volatility for a stock as an underlying.

Where can you find implied volatility of options?

Implied volatility is calculated from the market price of options, using the Black-Scholes option pricing model. Implied volatility for each F&O stock and Nifty/Bank Nifty can be easily observed in graphical as well as numerical form in Quantsapp’s IV suite.