Option traders don’t observe the same implied volatility across different strikes and different option types (call/put) on the same underlying (Nifty, Bank Nifty or F&O stocks) with the same expiry. Each and every option has a different implied volatility and when plotted looks like a smile, hence called volatility smile.

Ideas

Ideas

.svg)

Intel Junction

Trade

Trade

Orders API

Watchlist

Orders

Positions

Broker Access

Hot Keys

Alert Trigger Order (ATO)

Bracket Order

Target Stoploss Order

Add Broker

Track

Futures OI

Options OI

News

Price & Volume

Alerts

Built-Up Breadth

Built-Up Scrip Symbol

Synopsis Futures OI

Built-Up Sectors

Top Stocks

Intraday Movers

Analyze

Charts

IV

PCR

Expiry

Price & Volume

Charts/ Order & Trade

Multi Strike OI

O&T Watch List

Strategy Chart

Scan

Hist-Futures

Hist-Options

Pairs

Built-Up Scrip OI-Historical

Built-Up Sector Cycle

Built-Up Sector OI-Historical

Built-Up Scrip Cycle

Comparative Analysis

Tools

Easy Strategy

Strategy Builder

Quant Models

Essential Tools

Optimizer Find Strategy

Optimizer Find Specific

Optimizer My Forecasts

Optimizer Constrains

Learn

Live

Self Learning

Events

Webinars

Book a Session

Chapter 3

Volatility Skew

What is volatility skew or volatility smile?

Features of Volatility Skew

The two arguments raised by traders is that, why the shape of a smile and also, why the lowest point in the volatility smile is the implied volatility of the ATM option.

The implied volatility of ATM option, i.e. ATM IV is the lowest because of the very expectation of pricing in little or no movement for the underlying (Nifty, Bank Nifty, etc.), which means low expectation of volatility. Hence the IV is low at ATM, where the underlying is closed to that particular strike price of the options (call and put, both). One should remember that option trader is trying to incorporate the probability of the underlying, reaching close to the strike price, from its current price.

The extremes of the option chain, where the strike prices of options are at quite a distance from the ATM strike price, implies that for underlying to reach there even for a remote probability, the move (swing in prices) has to be large.

Let’s take an example: Nifty is quoting at 18500 and for a move to 19500 in two days, 1000-point transition, which means about 5.4% move in Nifty, in absolute terms. Though the probability or likelihood of this move is low, the expected volatility to achieve this would be much higher. So, for an option to turn from OTM to ITM or ITM to OTM, when its positioned far away from the current price of Nifty, entails discounting a larger expectation for volatility with a small probability of the occurrence of the event.

These two arguments result in volatility being different, at different strikes (call/put), for the same expiry and the same underlying. Hence the result is a curve popularly known as volatility smile or volatility skew.

Volatility skew for different asset classes

The extremes of the volatility smile have varied characteristics, depending on the asset class. From our previous chapter, we have learnt that a constructive move is slow in nature, while a destructive move is fast and with ferocity. So, its understandable that on the constructive extreme, the IVs are expected to be lower; as compared to IVs on the destructive extreme. As investors are likely to buy protection against the destructive move and hence would be buyer of options on those strikes, while on the constructive extreme, the need to buy protection isn’t a necessity. So, investors look to mitigate the risk (due to the destructive move).

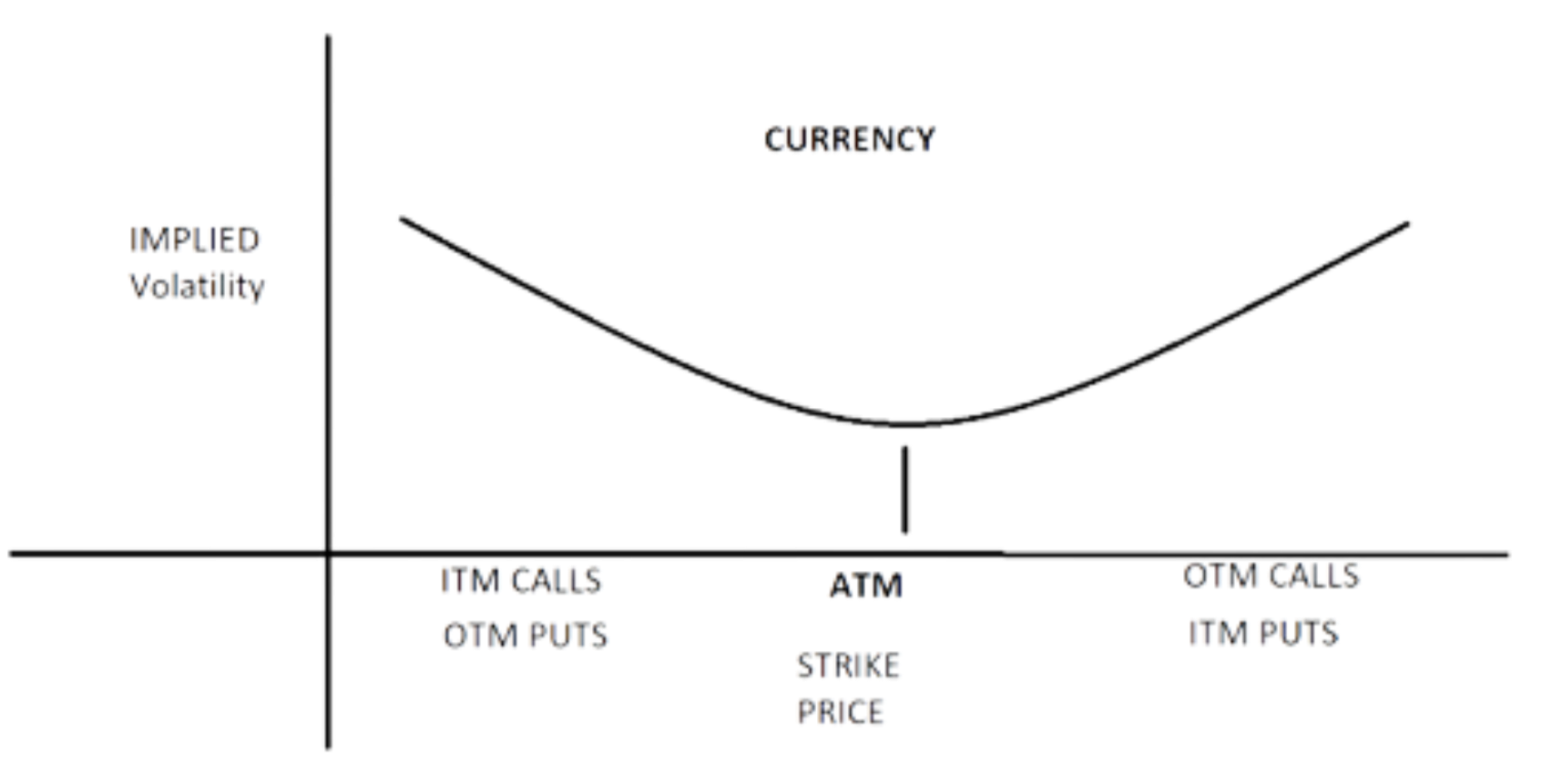

1. Volatility smile/skew for Currency options

In the case of Currency options, implied volatility used to price options at the two extremes tend to be higher than the ATM strike options, as a sharp move in currency on either side (appreciative or depreciative) hurts either exporters or importers. Hence the volatility smile is more symmetrical in this asset class, as the intensity of destructive move is equal on either extreme. The causes of volatility smile in case of currency options is due to the moves in currency which are characterised by jumps, rather than continuous changes.

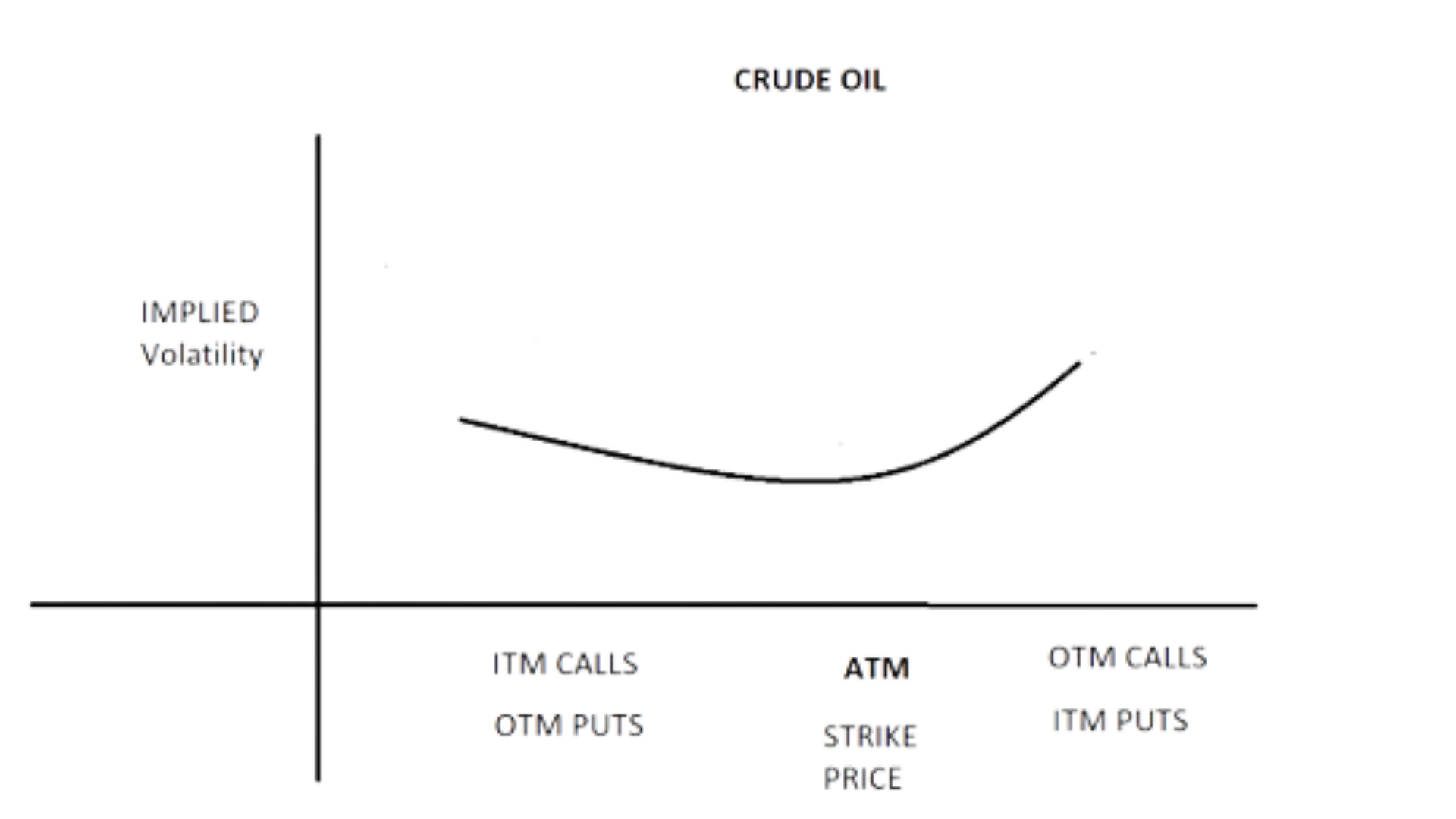

2. Volatility smile/skew for Crude oil options

The crude oil options’ implied volatility smile and its curvature is significantly influenced by hedging pressure on the underlying. The scarcity premium which could emanate due to supply issues tends to keep the higher strike prices at a higher implied volatility than the left extreme. With the ATM volatility being the lowest point of the smile or, rather, volatility skew, causing the right side of the curve to be tilted above, in comparison to the left side of the curve surrounding the ATM.

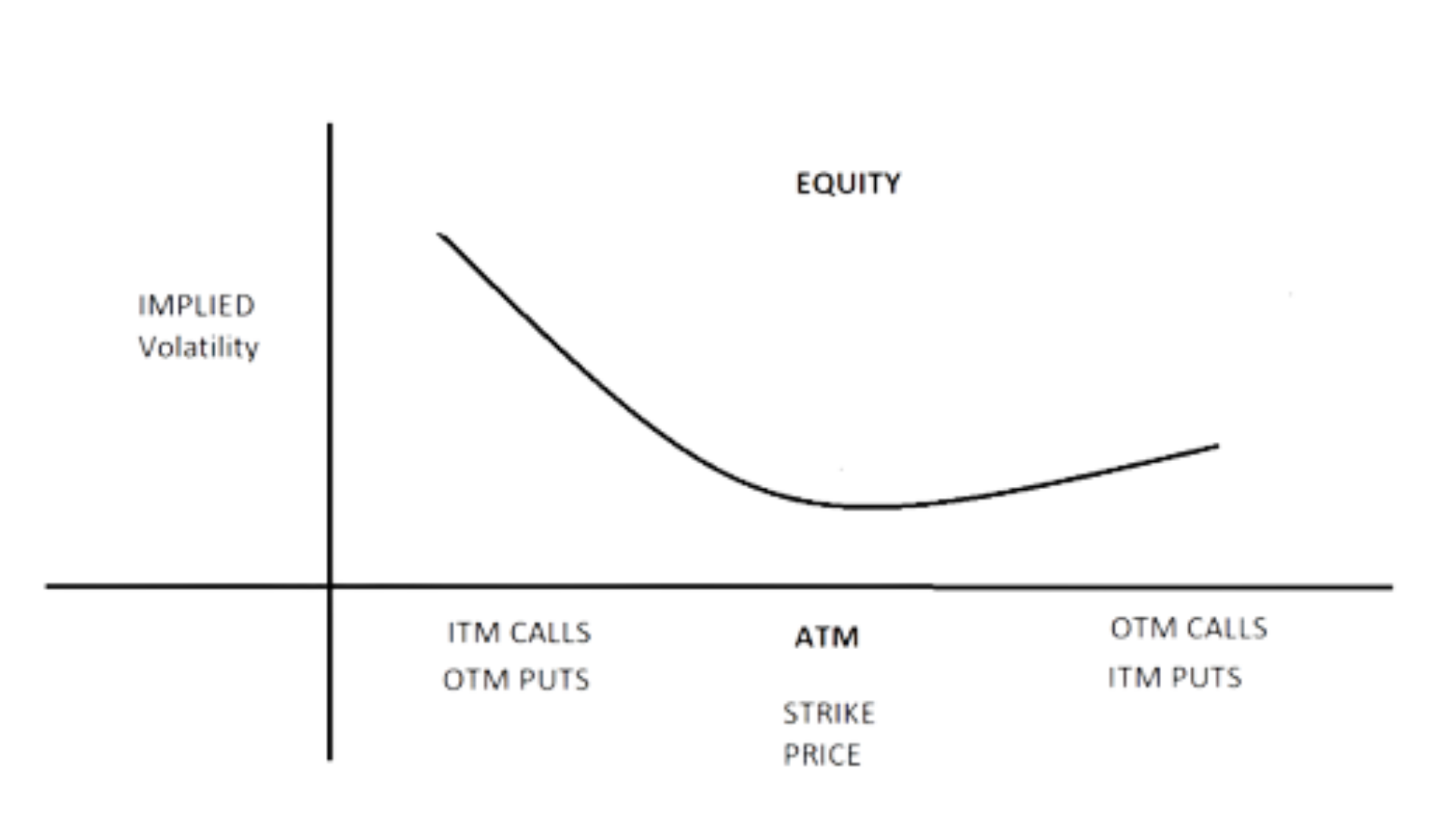

3. Volatility smile/skew for Equity options

In case of equity options, implied volatility used to price the lower strike price options is significantly higher, than those used for higher strike price options. This is because when the price of equity drops, there is more risk of destructive move, therefore options are bought, to hedge that destructive move. So implied volatility is higher during drops in strike price (i.e. left extreme) compared to the right extreme.

The Quantsapp volatility skew for NSE equity options, especially Nifty options is shown in the chart above. As mentioned earlier, the slope of the curve is steeper at lower strikes than the higher strikes. Quantsapp’s endeavour has been to provide cutting edge analytics in the Indian options market, to enable traders in their pursuit of being a data-driven trader.

Chart of Nifty Implied Volatility (IV) and Historical Volatility (HV). Note how in 2 major highlighted situations Implied Volatility rose first then dropped while Historical volatility rose later and dropped later.

FAQs

What does a volatility smile tell you?

The volatility smile indicates that implied volatility is lowest at the ATM strikes and is higher as one moves along the extremes.

What is the reason for the volatility smile?

The destructive moves in an underlying like Nifty, BankNifty or F&O stocks could be fast and ferocious, causing implied volatility to be higher on the lower extreme, than the higher extreme. This causes unequal volatility along the strikes of the options being studied. This takes the shape of a curve which is similar to a smile, hence the name, volatility smile.

What volatility smile is observed for equities?

Please note that the destructive move in equities could happen on the downward move, implying possible higher hedging demand for lower strikes than higher strikes, causing the implied volatilities along the lower extreme to be higher, than the higher extreme.