The drawback of the previous non-directional strategies was the potential of unlimited losses, hence the need to hedge the unlimited losses by purchase of suitable options which act as hedge and risk mitigation tools.

Ideas

Ideas

.svg)

Intel Junction

Trade

Trade

Orders API

Watchlist

Orders

Positions

Broker Access

Hot Keys

Alert Trigger Order (ATO)

Bracket Order

Target Stoploss Order

Add Broker

Track

Futures OI

Options OI

News

Price & Volume

Alerts

Built-Up Breadth

Built-Up Scrip Symbol

Synopsis Futures OI

Built-Up Sectors

Top Stocks

Intraday Movers

Analyze

Charts

IV

PCR

Expiry

Price & Volume

Charts/ Order & Trade

Multi Strike OI

O&T Watch List

Strategy Chart

Scan

Hist-Futures

Hist-Options

Pairs

Built-Up Scrip OI-Historical

Built-Up Sector Cycle

Built-Up Sector OI-Historical

Built-Up Scrip Cycle

Comparative Analysis

Tools

Easy Strategy

Strategy Builder

Quant Models

Essential Tools

Optimizer Find Strategy

Optimizer Find Specific

Optimizer My Forecasts

Optimizer Constrains

Learn

Live

Self Learning

Events

Webinars

Book a Session

Chapter 8

Hedged Non-Directional Strategies

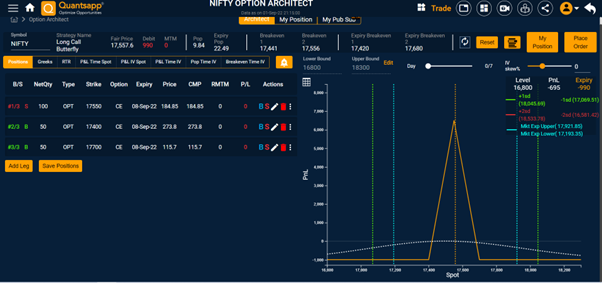

Long Call Butterfly

A long call butterfly spread is a four-leg strategy that is created by buying one call at a lower strike price, selling two calls with a higher strike price and buying one call with an even higher strike price. All calls have the same expiration date, and the strike prices are equidistant.

The maximum profit is arrived at when the stock price is equal to the strike price of the short calls (centre strike) on the date of expiration of option contracts. The maximum risk/loss is the net cost of the strategy realised; if the stock price is above the highest strike price or below the lowest strike price at expiry.

Consider a Long Call Butterfly where Nifty Futures Fair value is quoting at 17,558, trader shall

Buy 17700 8 Sep 2022 CE at 115.70

Sell 17550 8 Sep 2022 CE at 184.85

Sell 17550 8 Sep 2022 CE at 184.85

Buy 17400 8 Sep 2022 CE at 273.80

The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,420 and Expiry BEP2 of the strategy is at 17,680.

The entire option premium collected for the two legs less two hedges purchased, is the maximum profit. The maximum profit is possible, if, Nifty stays at the centre strike; losses are capped above 17700 and below 17400.

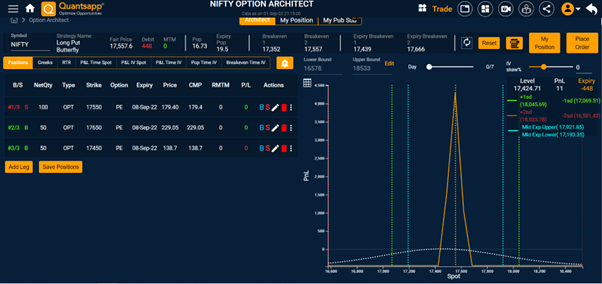

Long Put Butterfly

A put butterfly, also known as a long-put butterfly, is a four-leg, neutral strategy with limited profit potential and limited pre-defined risk. The put butterfly has four put option components with the same expiration date: two short puts are sold at the same strike price, one long put is purchased above the short strikes, and one long put is purchased below the short strikes. A put butterfly is a combination of a bear put debit spread and a bull put credit spread at the same strike price. The long put options are at the same price gap (of strike prices) from the short put options.

The initial amount paid to enter the put butterfly strategy is the maximum defined risk. The profit potential is limited to the difference between the long and short strikes less the initial amount paid. The strategy looks to take advantage of a drop in volatility, time decay, and little or no movement from the underlying asset (oscillating regime).

Consider a Long Put Butterfly where Nifty Futures Fair value is quoting at 17,558, trader shall

Buy 17650 8 Sep 2022 PE at 229.05

Sell 17550 8 Sep 2022 PE at 179.40

Sell 17550 8 Sep 2022 PE at 179.40

Buy 17450 8 Sep 2022 PE at 138.70

The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,439 and Expiry BEP2 of the strategy is at 17,666.

The entire option premium collected for the two legs, less two hedges purchased, is the maximum profit. The maximum profit is possible, if, Nifty stays at the strike of the middle component of the strategy and losses are capped above 17700 and below 17400.

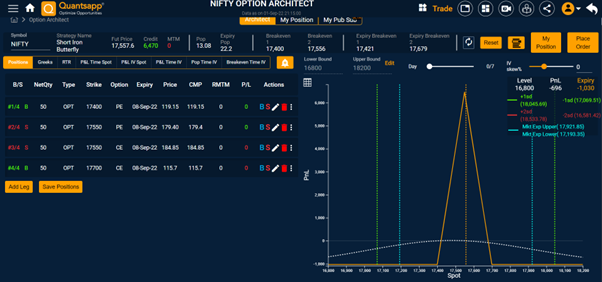

Iron Butterfly

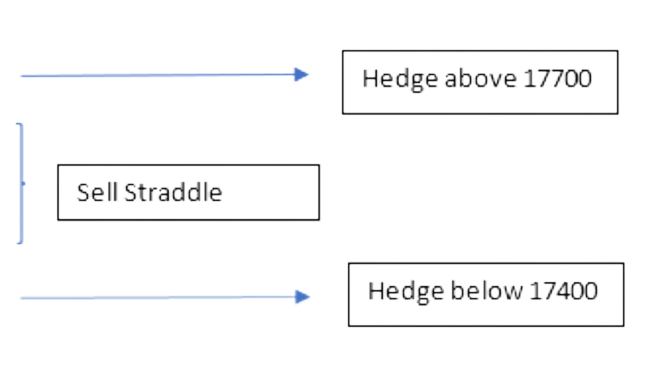

Iron butterfly option strategy is a modification to a short straddle option strategy which is used in an oscillating market. But the drawback of a short straddle or a sell straddle is unlimited losses which needs to be truncated, by buying of OTM call and OTM put. A call and put are both sold at the middle strike price i.e. a short straddle, which forms the “body” of the butterfly, and a call and put are purchased above and below the middle strike price, respectively, to form the “wings” to hedge the unlimited losses and cap them at a particular level. The iron butterfly strategy can generate steady income while limiting risks and profits, especially with option premia collected from the sale of the straddle, reduced by the purchase of option hedges on either side of the straddle strike price.

consider a short iron butterfly where Nifty Futures Fair value is quoting at 17,558, trader shall

Buy 17700 8 Sep 2022 CE at 115.70

Sell 17550 8 Sep 2022 CE at 184.85

Sell 17550 8 Sep 2022 PE at 179.40

Buy 17400 8 Sep 2022 PE at 119.15

The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,421 and Expiry BEP2 of the strategy is at 17,679.

The entire option premium collected for the two legs is the maximum profit, less the two hedges purchased. The maximum profit is possible, if, Nifty stays at the strike of the straddle component of the strategy and losses are capped above 17700 and below 17400.

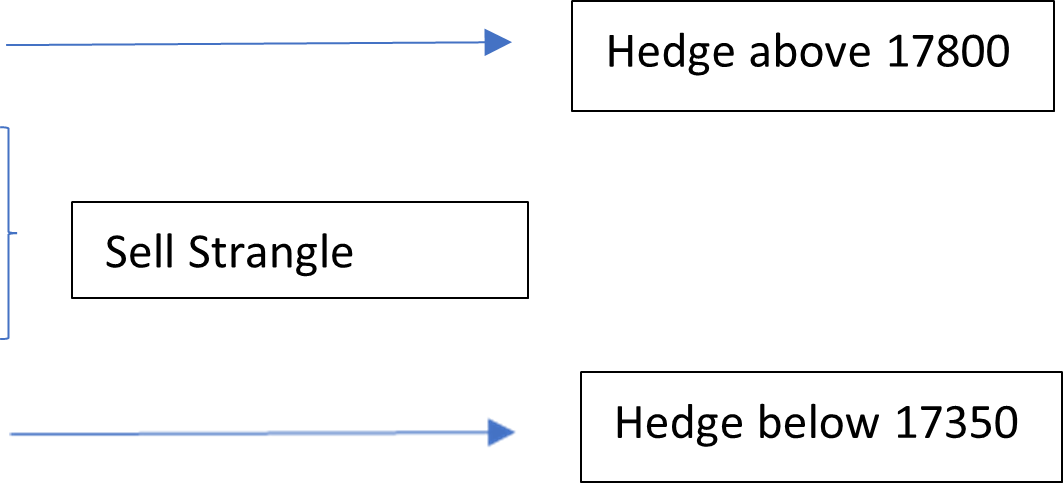

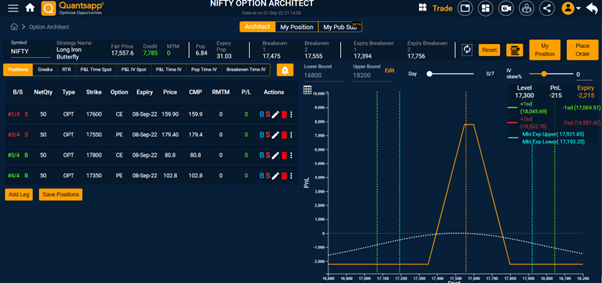

Iron Condor

Iron condor option strategy is a modification to a short strangle option strategy which is used in a slightly wider oscillating market. But the drawback of a short strangle or a sell strangle is unlimited losses which needs to be truncated, by buying of a further OTM call and OTM put. A call and put are both sold at OTM strikes, slightly spread apart, similar to that in a sell strangle and a call and put are purchased farther above and below the middle strike price, respectively, to form the “wings” to hedge the unlimited losses and cap them at a particular level. The iron condor strategy can generate steady income while limiting risks and profits, especially with option premia collected from the sale of the straddle, reduced by the purchase of option hedges on either side of the straddle strike price.

The maximum profit for an iron condor is the amount of premium, or credit, received for creating the four-leg options position, i.e. short strangle and purchase of wings. The maximum loss occurs if the price moves above the long call strike, which is higher than the sold call strike, or below the long put strike, which is lower than the sold put strike and is capped. The maximum loss is the difference between the long call and short call strikes, or the long put and short put strikes. The loss is reduced by the net credits received, to give the net loss. This is under the hypothesis that the prices of the underlying would be ranged, albeit slightly wider than in the case of an iron butterfly.

Consider a short iron condor where Nifty Futures Fair value is quoting at 17,558, trader shall

Buy 17800 8 Sep 2022 CE at 80.80

Sell 17600 8 Sep 2022 CE at 159.90

Sell 17550 8 Sep 2022 PE at 179.40

Buy 17350 8 Sep 2022 PE at 102.80

The expiry payoff is indicated in orange colour. Expiry BEP1 of the strategy is at 17,394 and Expiry BEP2 of the strategy is at 17,756.

The entire option premium collected for the two legs, less purchase of the wings (hedges) is the maximum profit. The maximum profit is possible, if, Nifty stays between the two strikes of the strangle component of the strategy and losses are capped above 17800 and below 17350.

FAQs

Is hedging an option strategy good?

If an option strategy entails the possibility of unlimited losses, hedging it by buying OTM strike options reduces risk, but at the cost of forgoing some profitability. These are low risk strategies and suitable for traders who don’t wish to take unlimited risk, which is accompanied with naked option selling.

How many put call options do we use in butterfly strategy?

Long call butterfly involves the combination of 1 CE of a lower strike, selling 2 CE of a middle strike and buying 1 CE of an even higher strike price; with the middle strike being equidistant from the lower and higher strikes. This strategy involves 4 legs. Long put butterfly involves the combination of 1 PE of a lower strike, selling 2 PE of a middle strike

and buying 1 PE of a higher strike price; this strategy involves 4 legs, with same expiry and equidistant.

What is the difference between long put butterfly and long call butterfly?

Long call butterfly involves the combination of 1 CE of a lower strike, selling 2 CE of a middle strike and buying 1 CE of an even higher strike price; with the middle strike being equidistant from the lower and higher strikes. This strategy involves 4 legs. While long put butterfly is a similar strategy but is created or formulated using puts only. It is also a 4 leg strategy.

What is a long butterfly option strategy?

Butterfly strategy can be constructed using only calls or only puts, illustrated ahead:

Long call butterfly involves the combination of 1 CE of a lower strike, selling 2 CE of a middle strike and buying 1 CE of an even higher strike price; with the middle strike being equidistant from the

lower and higher strikes. This strategy involves 4 legs. Long put butterfly involves the combination of 1 PE of a lower strike, selling 2 PE of a middle strike and buying 1 PE of a higher strike price; this strategy involves 4 legs, with same expiry and equidistant.

Is iron condor always profitable?

Iron condor strategy is profitable when the underlying expires within a pre-defined range which is dependent on the option strikes used in formulating the iron condor.