.svg)

Volga is a second-order option Greek that measures the rate of change of vega (the option's sensitivity to changes in implied volatility) with respect to changes in implied volatility. Volga is also known as "Vomma".

Volga is important because it tells traders how much an option's value will change as the implied volatility changes. If an option has a high Volga, its value will be more sensitive to changes in implied volatility, which means that the option will be more expensive or less expensive depending on the volatility levels.

Like other option Greeks, Volga can be used to manage risk in options trading. Traders can use Volga to adjust their positions to changes in implied volatility, which can help them to protect their portfolios from adverse moves in the market.

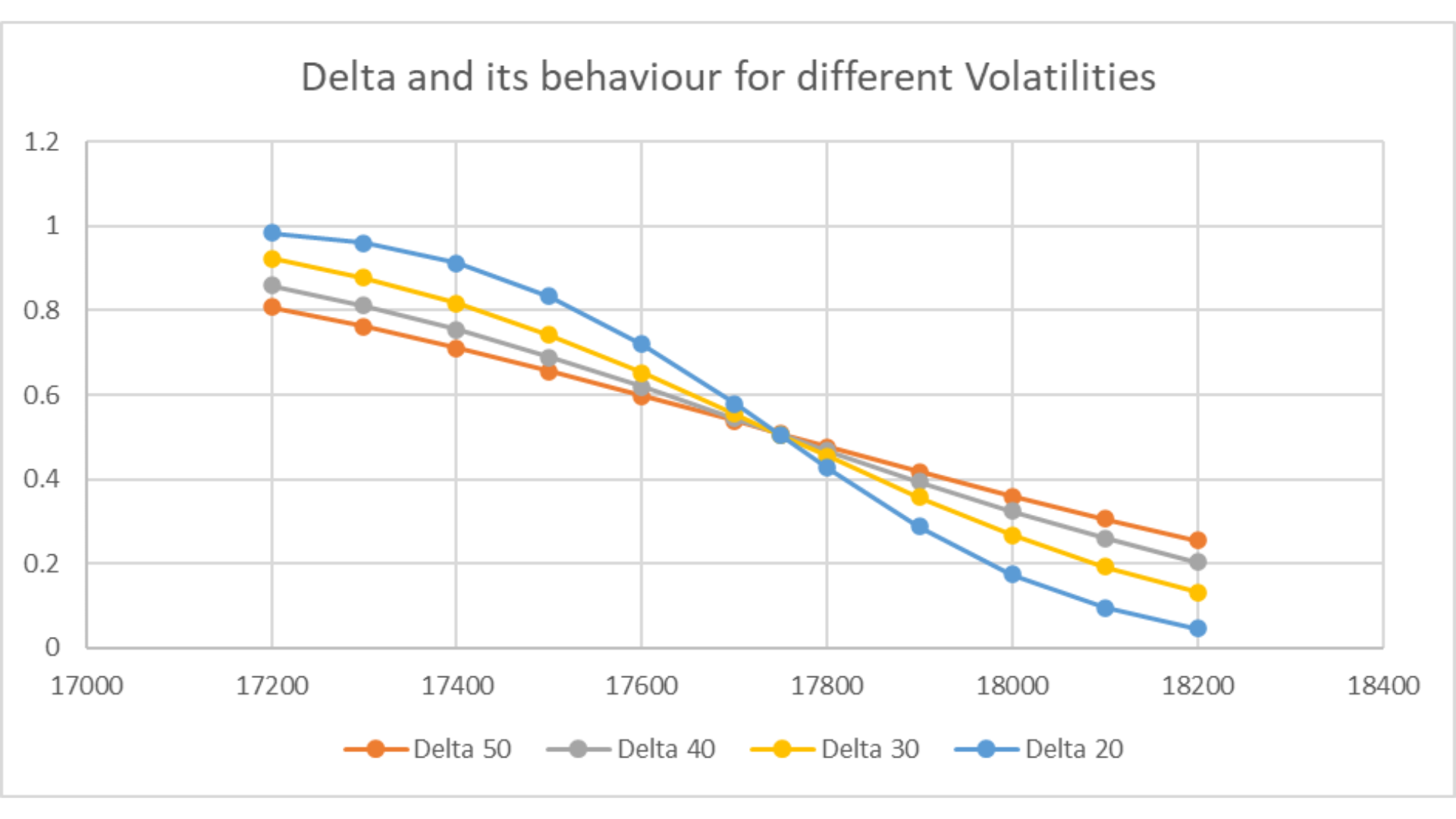

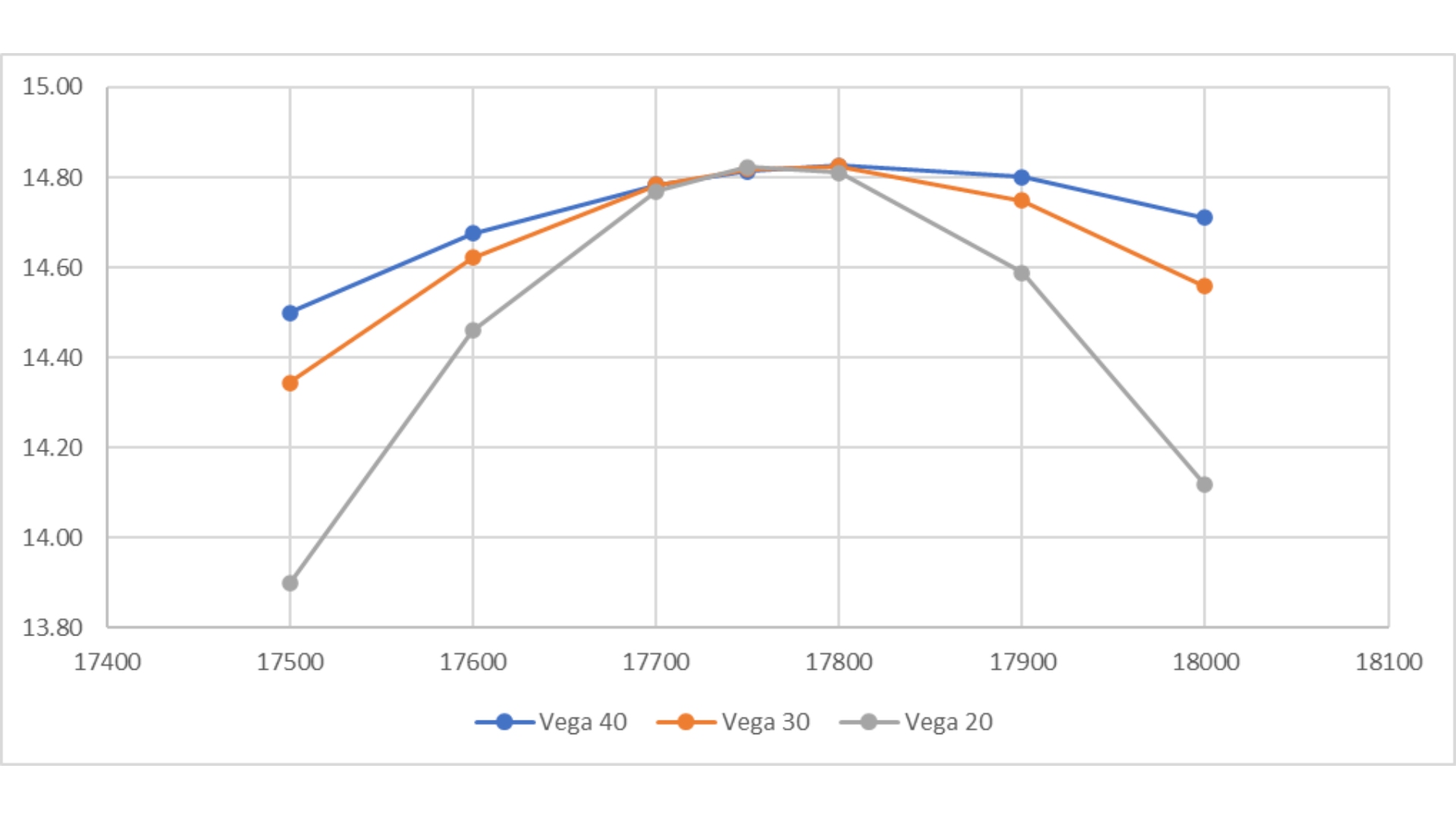

The chart ahead indicates the vega values for different implied volatilities, with vega 40 indicating Nifty option vega at 40% volatility, so on. Days to expiry for the option is 2 days, for ATM strike = 17750.

Nifty Options

Days to expiry (DTE) = 2

ATM strike = 17750

Similarly, the second chart indicates Nifty option vega at different implied volatilities with DTE = 16.