.svg)

As they say,

Time is Ticking Away!

We are aware that options as financial instruments are speculative instruments and not investment vehicles. They have an expiry date and are inexistent, post that.

The value of an option can be analysed into two parts (as discussed earlier):

the intrinsic value

and

the time value.

The intrinsic value is the amount of money you would gain if you exercised the option immediately, so a call with strike Rs 50 on a stock with price Rs 60 would have intrinsic value of Rs 10, whereas the corresponding put would have zero intrinsic value.

The time value is the value of having the leisure or opportunity of waiting longer before deciding to exercise. Hence its necessary to understand theta in options trading to have effective option trading strategies.

An extreme deep OTM option on Nifty (call or put) may quote a really low value (non – zero), few days before expiry as there exists an iota of chance that Nifty might touch that strike price (assuming, if a really large price swing were to occur in the remnant time period). Once the option heads to maturity or is just about to expiry, the time left for the option is inexistent and therefore the time value in the option reduces to zero and the option premium is only the intrinsic value of the option, which we all are aware that for OTM options is 0 (zero).

Thus, if you are long an option your portfolio theta is negative: your portfolio will lose value with the passage of time (all other factors held constant).

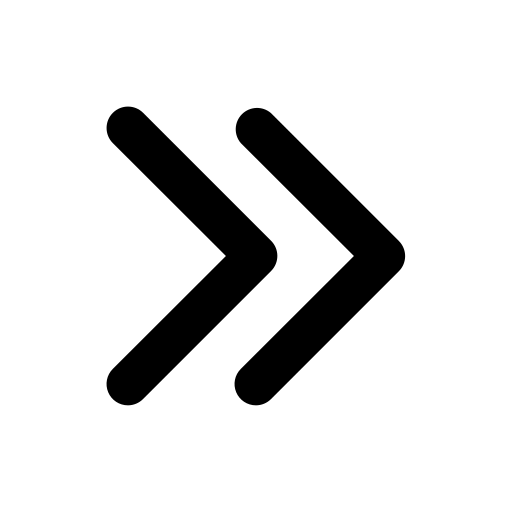

Options’ Theta measures the sensitivity of the value of the derivative to the passage of time or time decay. Option Greek, Theta, represents the sensitivity of the option's value to changes in time. A first order Greek, which is negative, means that the option's value will decrease as time passes, while a positive theta means that the option's portfolio will increase as time passes. Option Theta decay refers to the natural decrease in the value of an option as time passes and the option approaches expiration, assuming all other factors remain constant.

Theta is almost always negative for long calls and puts, and positive for short (or written) calls and puts.