.svg)

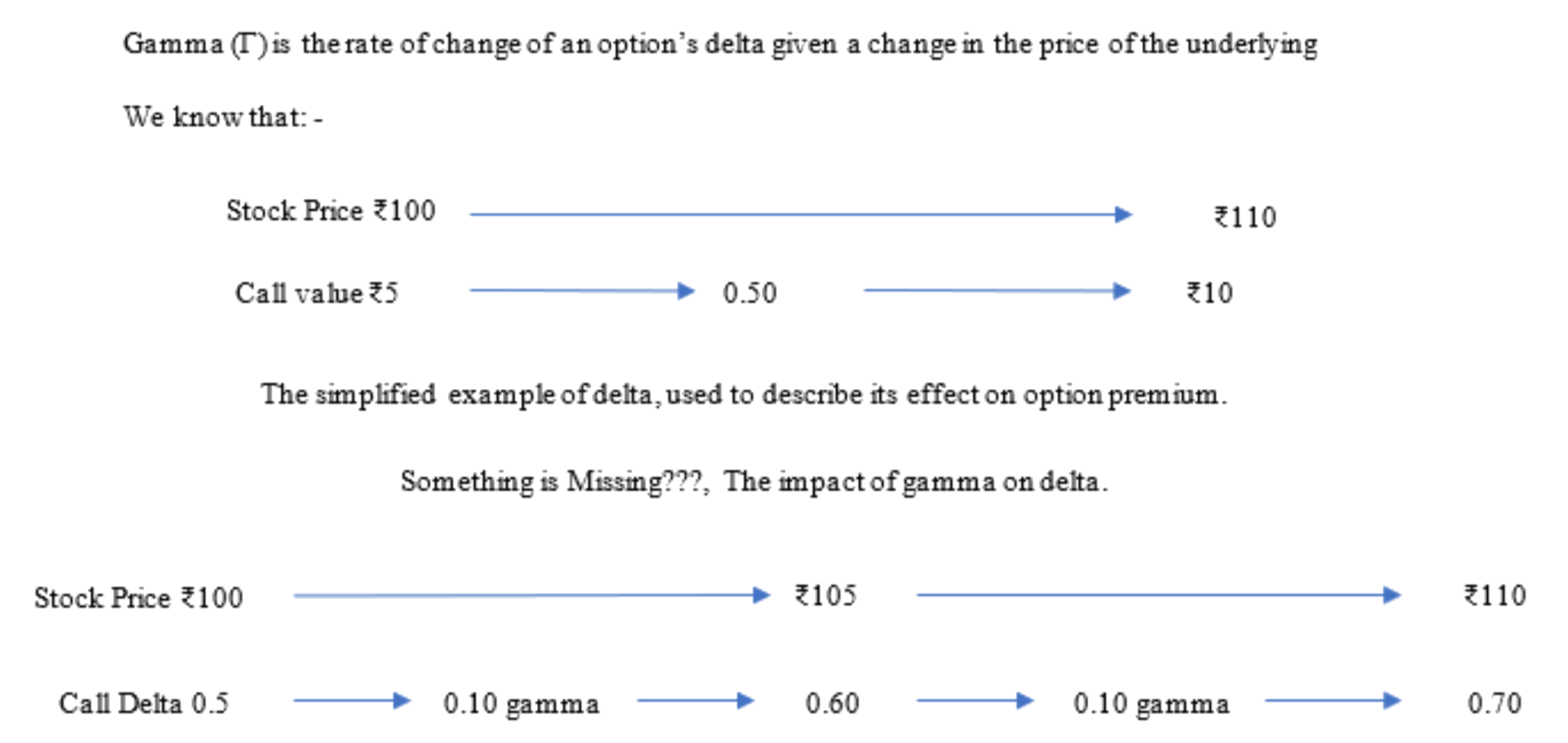

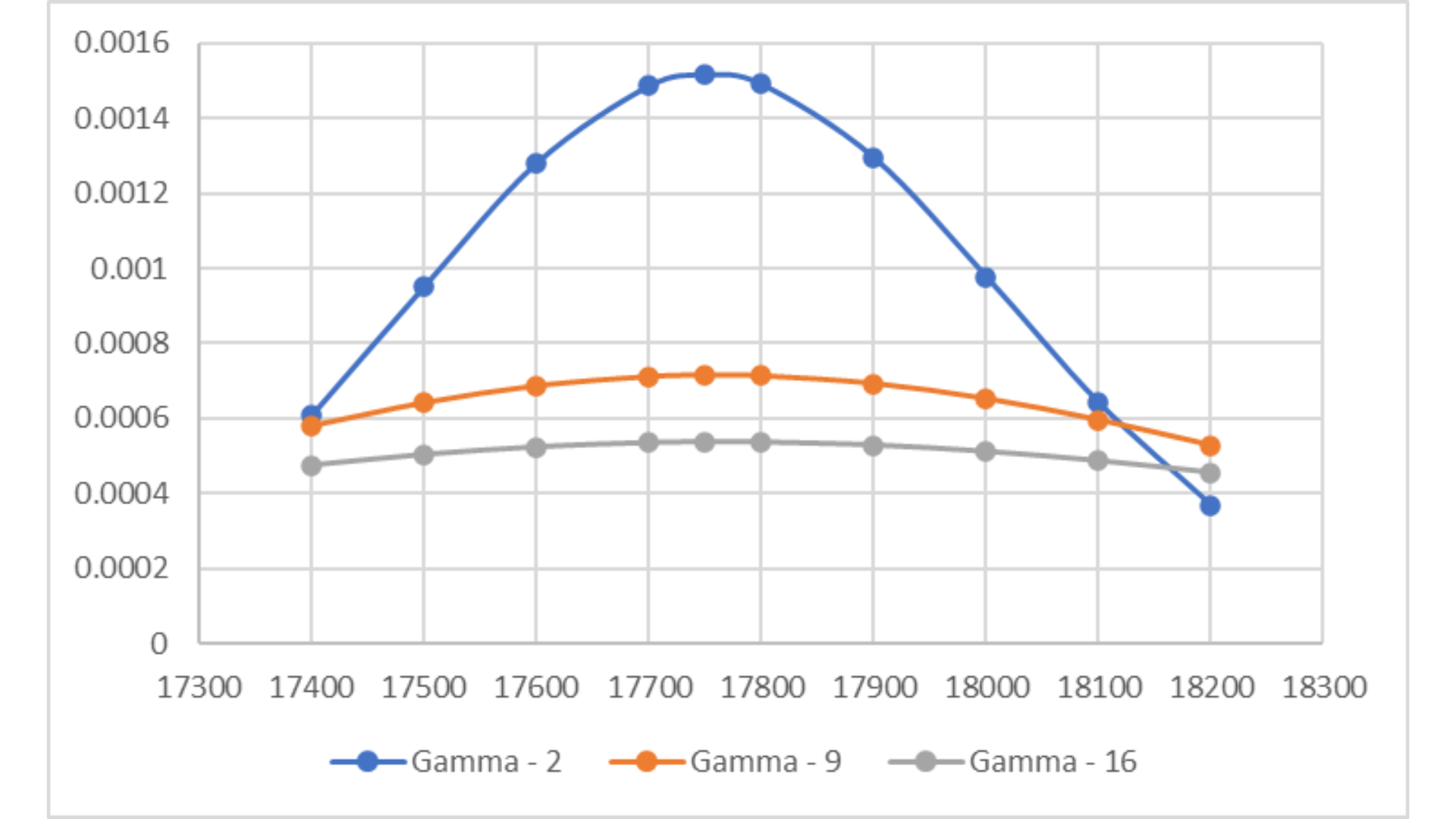

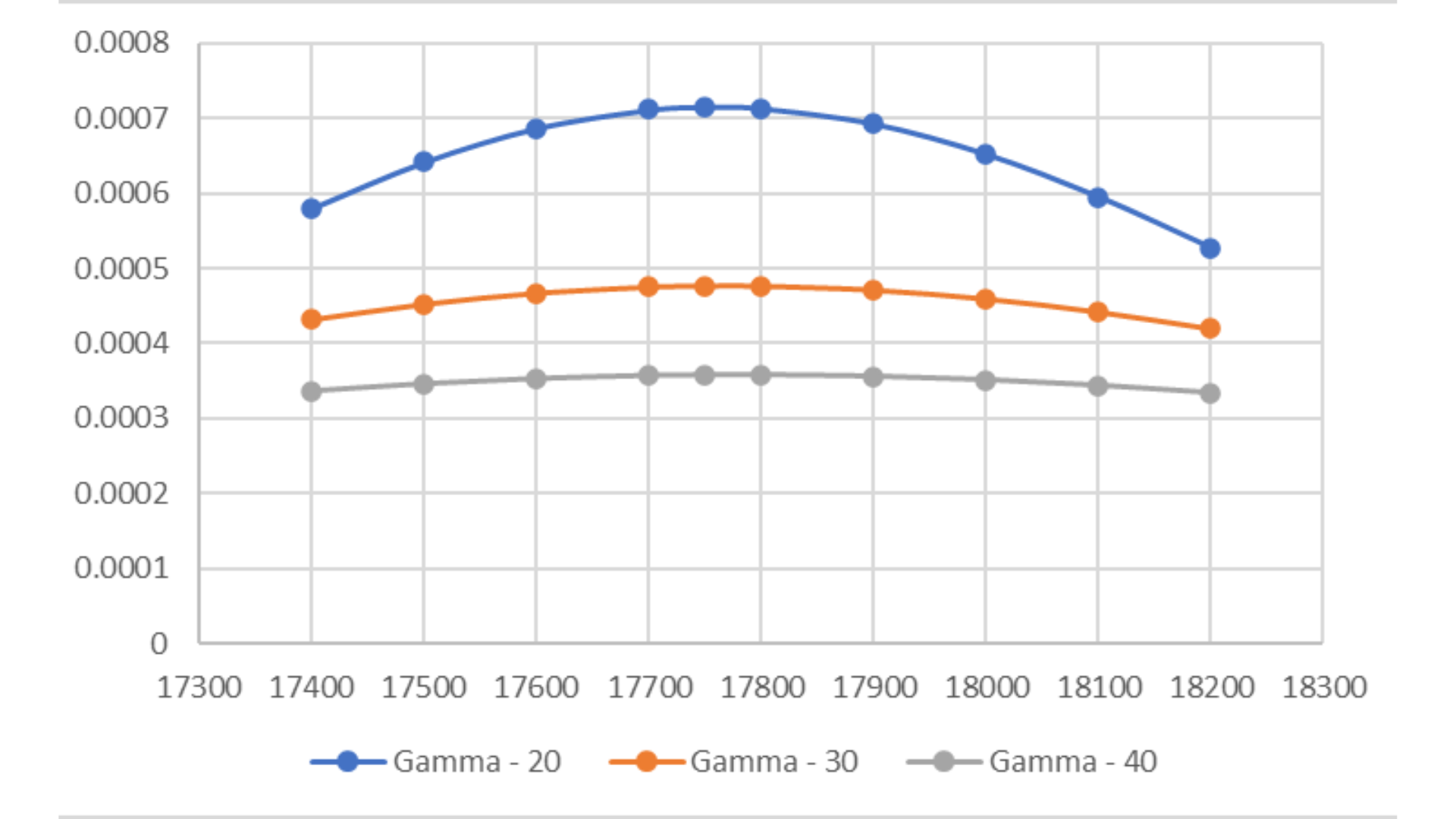

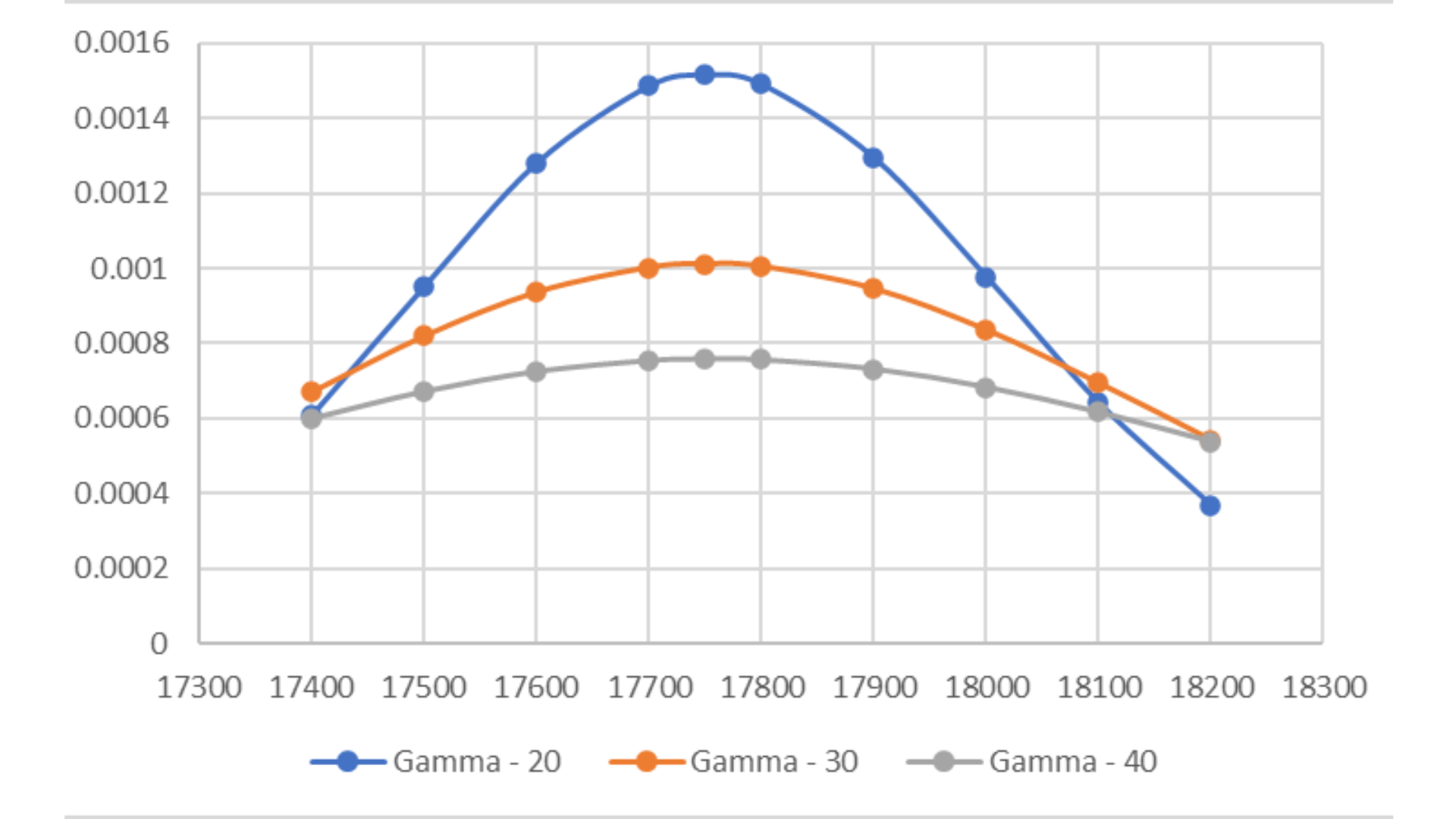

Gamma is a second-order Greek in options trading and refers to the rate of change of an option's delta per unit change in the underlying asset's price.

Gamma is a crucial Greek to understand when managing an options portfolio, as it helps traders anticipate the potential impact that changes in the price of the underlying asset will have on the option's delta and, as a result, its potential profitability. A positive gamma means that an option's delta will increase as the underlying asset's price rises, and decrease as the underlying asset's price falls. A negative gamma means the opposite, with the option's delta decreasing as the underlying asset's price rises and increasing as the underlying asset's price falls.