.svg)

Stock prices don't move in a preconceived path. Of course, financial analysts put forth forecasts about a particular sector or asset to reach certain price targets. These forecasts may be right or may prove to be wrong later, but that’s not the matter of contention for us.

The path for prices of Nifty may be currently quoting at 18000; let’s assume it is forecasted by market experts to move to 19000 over the period of 1 year. Inspite of the forecasted target of the stock, or index like Nifty (underlying), the path, price takes over the period of 1 year is unknown. Nobody knows, Would the index go to 16000 first and then move to about 19000, later, or would the prices move to 19000 directly in a gusto move; or would the prices meander about the current price 18000 to then, transition to 19000?

Even Black-Scholes option pricing model is a mathematical model used in pricing of options, giving a theoretical estimate for European-style options. This model, also, assumes the stock prices (or underlying prices) follow a geometric Brownian motion, a pattern of motion typically consists of random fluctuations in a particle's position inside a fluid sub-domain.

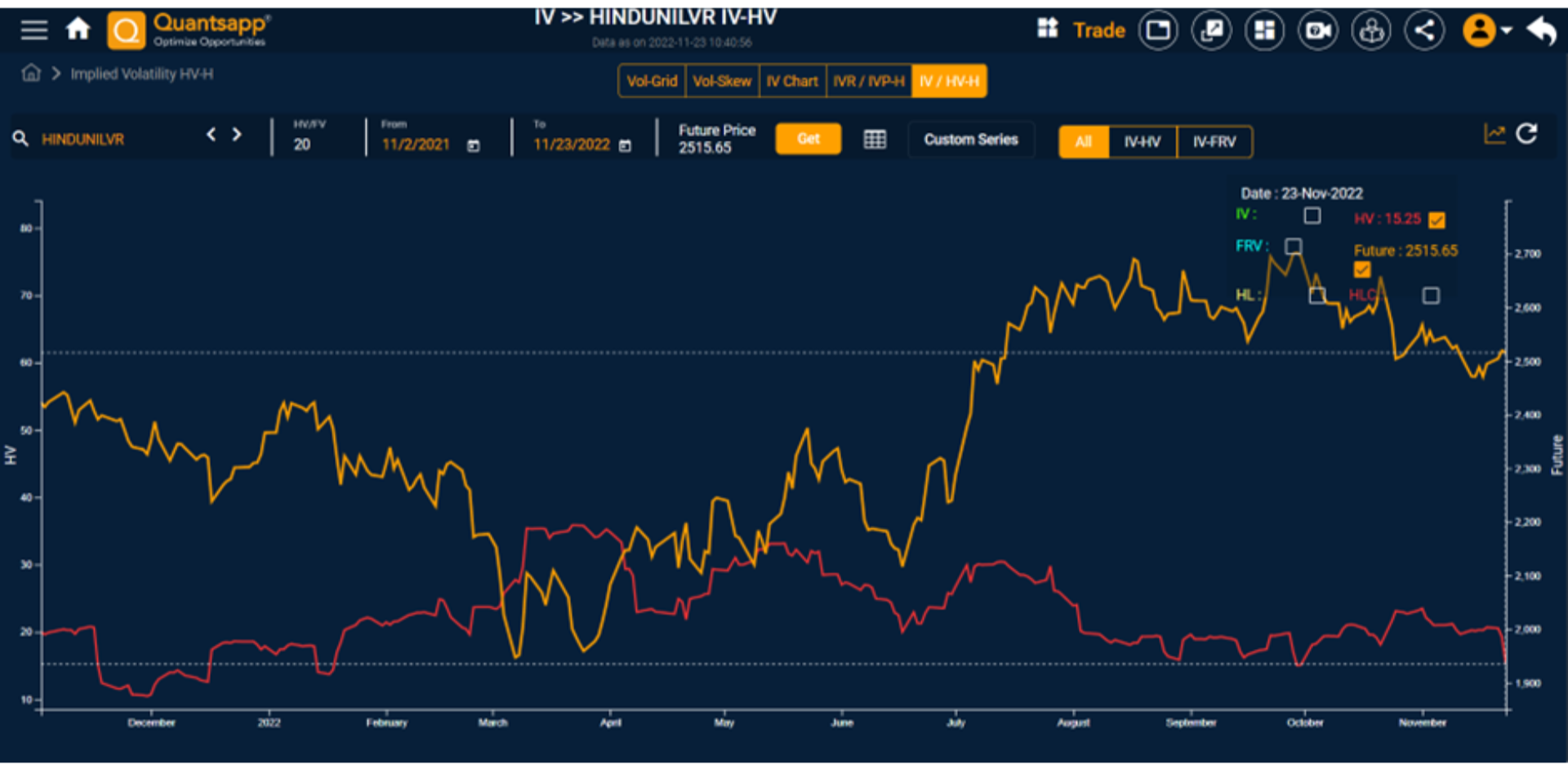

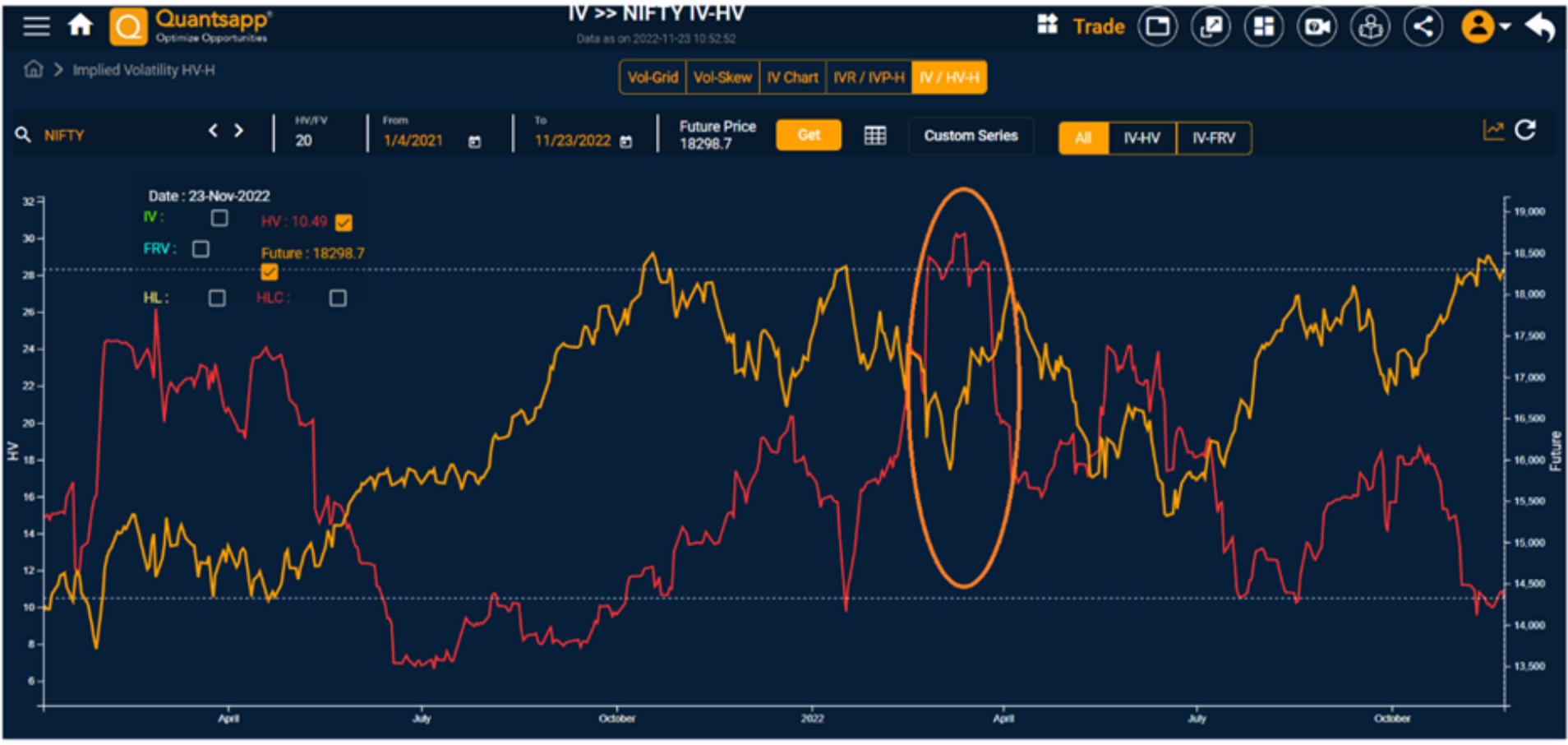

Volatility is nothing but the Path Taken. So, learning volatility and its impact on option pricing is pivotal for option traders.